If your home insurance renewal arrived this year with a number that made you do a double-take, you’re not imagining things — and you’re not alone.

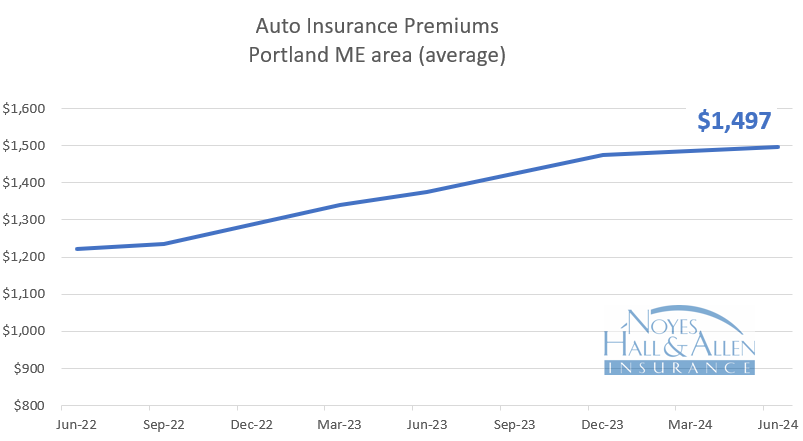

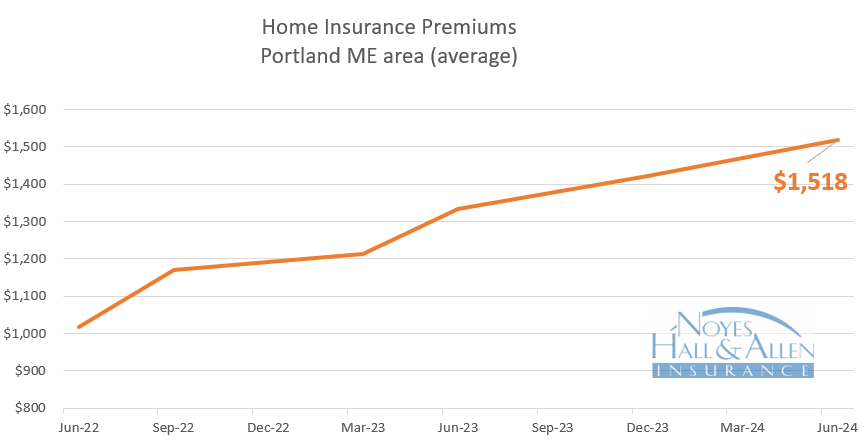

Home insurance premiums across Maine have increased significantly over the past several years. Before you assume there’s nothing you can do, it helps to understand why it’s happening and what your options actually are — especially if you’re working with an independent insurance agent in Maine who can shop the market on your behalf.

Why Is Maine Home Insurance Getting More Expensive?

The short answer: insurance is priced on risk, and the cost of risk has risen sharply nationwide — even in places that haven’t had major local losses.

Rising Reinsurance Costs

Insurance companies buy insurance too — it’s called reinsurance, and it protects them from catastrophic loss years. After a stretch of expensive hurricane seasons, wildfires, and severe storms across the country, reinsurance prices spiked. Maine insurers pay those higher costs, and some of that flows to your renewal.

Higher Construction and Repair Costs

Replacing a damaged home costs a lot more today than it did five years ago. Labor and materials — especially lumber — saw sharp inflation post-pandemic. Your homeowners insurance in Maine needs to reflect what it would actually cost to rebuild your home today, not what it cost when your policy was first written. Many carriers have adjusted replacement cost estimates upward, which increases the premium.

Carrier Underwriting Changes

Some insurance companies have pulled back from certain markets or tightened their eligibility requirements. When carriers reduce their appetite, competition shrinks — and prices reflect that. This is especially relevant in Maine, where fewer carriers compete for certain types of homes and locations.

What Can Mainers Do About Rising Home Insurance Costs?

None of the factors above are your fault. But you shouldn’t simply accept a renewal you haven’t had anyone review. Here’s what’s worth knowing.

Work With an Independent Agent Who Shops for You

If you buy home insurance directly from a single company — online or through a captive agent — your only real option when the price goes up is to accept it, reduce your coverage, or start over somewhere else on your own.

When you work with an independent insurance agency like Noyes Hall & Allen in South Portland, Maine, you have someone who represents multiple carriers. That matters at renewal time.

We review our clients’ renewals and actively shop their coverage when rates move in ways that don’t make sense. If your current carrier has raised your Maine homeowners insurance premium and another company we represent can offer comparable coverage at a better price, we’ll find it. If your current carrier is still your best option, we’ll tell you that honestly — and explain why.

Make Sure Your Coverage Still Makes Sense

A renewal is also a good time to review what you actually have. Some homeowners are paying for coverage limits or options that no longer fit their situation. Others are underinsured and don’t realize it. A review with your agent can identify both.

Be Careful About Cutting Coverage to Save Money

It can be tempting to raise your deductible or drop optional coverages to offset a premium increase. Sometimes that’s the right call — but not always. Before you make changes, talk to an agent who can walk you through the tradeoffs. Saving $100 a year on your premium isn’t a good deal if it leaves you with a $5,000 gap after a claim.

Why Greater Portland Homeowners Work With Noyes Hall & Allen

Noyes Hall & Allen has been helping Maine homeowners navigate the insurance market since 1928. We’re an independent agency in South Portland, which means we’re not locked into one carrier’s products or pricing. We represent close to 20 insurance companies and our job is to find the right fit for you — not to push one company’s product.

When your renewal arrives, you shouldn’t have to figure out on your own whether it’s fair. That’s what we’re here for.

Get a Second Opinion on Your Maine Home Insurance Renewal

If your homeowners insurance renewal is coming up — or if you’ve already renewed and are still frustrated by the price — reach out to us. Bring your current declarations page if you have it. We’ll take a look at what you have, what you’re paying, and whether there’s a better option available in the Maine market.

Call us at 207-799-5541, text us at 207-517-4065, or request a home insurance quote online.