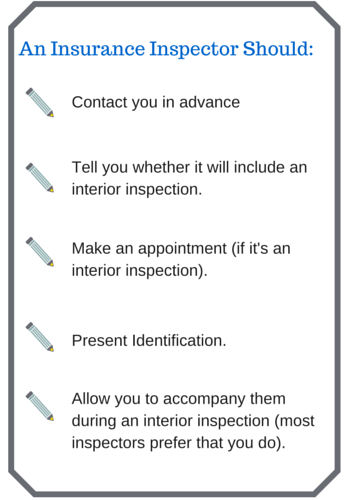

Insurance policies give insurance companies the option to inspect your property from time to time. The result of your insurance property inspection is a report to the company underwriter.

If the underwriter has concerns, they make “recommendations” to address them. This is a euphemism. These are not recommendations at all, but requirements. A “recommendation” may be as minor as fine-tuning the amount of insurance on your property (up or down); or as major as replacing the roof.

The underwriter sets a deadline for the “recommendation” to be completed. The deadline varies depending on the severity of the situation, how long they’ve insured your property, when your policy expires, and the season of year.

The Importance of Communication

The worst thing you can do is ignore an insurance company “recommendation”. Nobody likes to be  ignored; insurance underwriters dislike it more than most. It’s better to let the insurance company know your intentions, or to ask questions if you don’t understand.

ignored; insurance underwriters dislike it more than most. It’s better to let the insurance company know your intentions, or to ask questions if you don’t understand.

Your Maine insurance agent is the link between you and the insurance company. Talk to them! They can explain the situation and advocate for you. If you are uncertain what the underwriter requires and why, ask your agent for a clarification. If you are unable to comply or need help, tell your agent. Depending on the circumstances, your agent may be able to negotiate with the underwriter for more time or for a different solution to the issue.

If the insurer’s recommendation involves physical changes to your property, they will require confirmation that you’ve made them. This usually means sending a photo of the completed change. The company may ask for a signed statement confirming that the change is permanent (such as removing a trampoline from the yard).

What Happens If You Can’t – or Won’t – Comply With Insurance Company Inspection Recommendations?

If the underwriter’s deadline passes without confirmation that the recommended changes were made, they may cancel your policy. Depending on the severity of the recommendation, they may cancel your policy within 30-45 days, or send a notice of non-renewal for when the policy expires.

When your policy is canceled or non-renewed by an underwriter, it’s very difficult to obtain replacement insurance with a preferred company. Your agent may be able to find replacement coverage, but it will probably at a higher cost and with less broad coverage.

Also, remember that you’re then a new customer with another insurance company. Now THEY may want to inspect. The cycle begins again, and it’s not always a good cycle.

If you have a question about Greater Portland Maine home or investment property insurance, contact a Noyes Hall & Allen agent in South Portland at 207-799-5541. We offer you a choice of Maine’s preferred property insurance companies. We’re independent and committed to you.