Almost every state in the U.S. requires drivers to have car insurance. Like every other law, there are always some people who choose to ignore or disobey it.

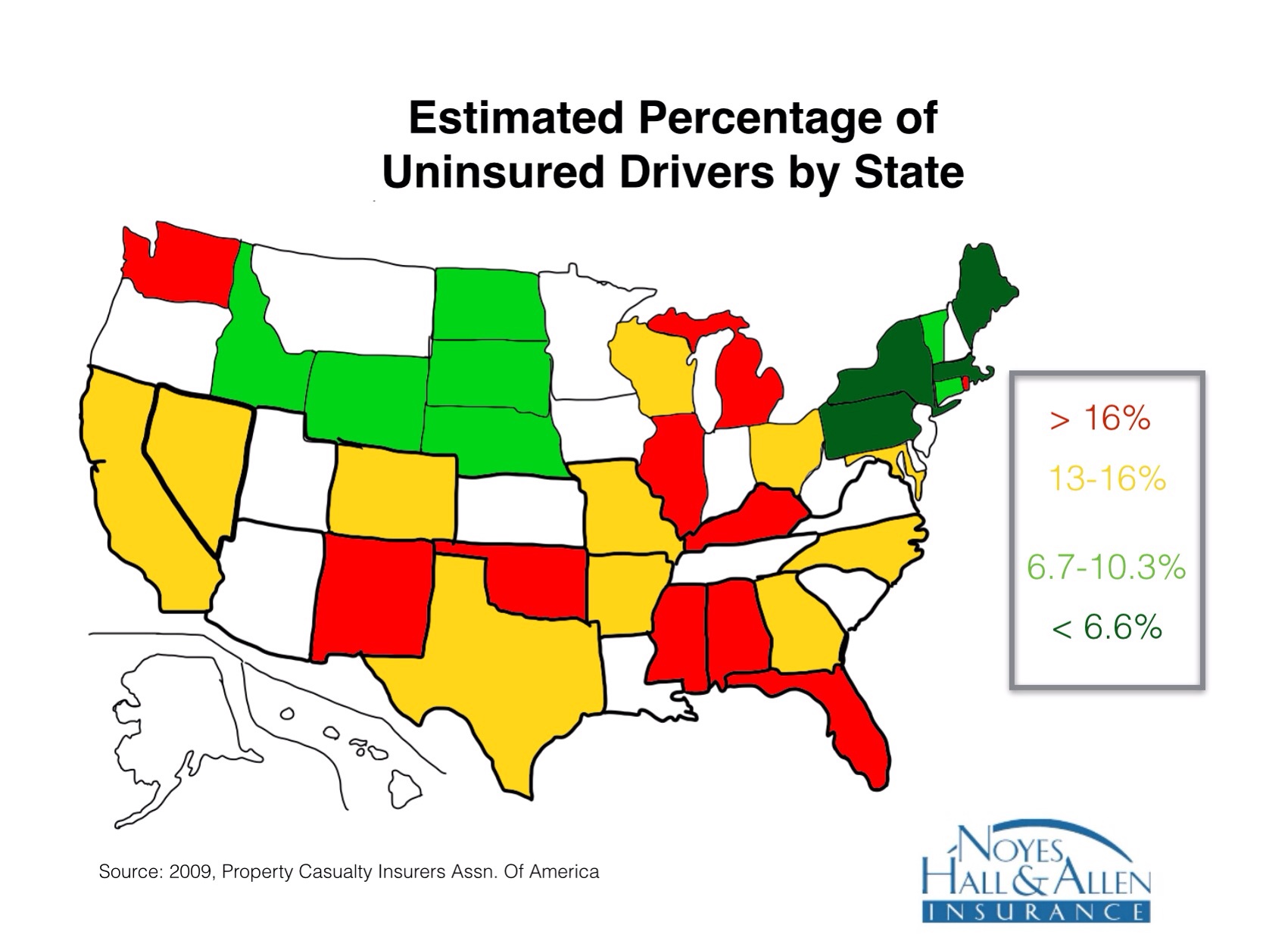

The good news: if you are in a crash in Maine, the other driver probably has insurance. Maine is in the Top 10 states for percentage of insured drivers.

The bad news: many Maine drivers carry very low liability limits – as low as $50,000 per person. After an accident, your medical expenses can easily exceed that.

What if the Other Driver Doesn’t Have Enough Insurance to Pay My Damages?

It’s great if the at-fault driver has insurance. Do they have enough insurance to pay your damages? Who knows? At 50/100/25, Maine’s minimum auto liability insurance limits are among the highest in the country. But if you drive a late-model car, $25,000 isn’t going to replace it. If you are badly injured, you can accumulate $50,000 in medical bills in one day. You need to protect yourself.

What Happens if Someone Hits Me and They Don’t Have Insurance?

If an uninsured driver hits you, you have to rely on your own Maine auto insurance. Your collision coverage (if you purchased that option) will pay to repair your vehicle. If you don’t carry collision insurance, you’ll have to deal with the damages on your own. Some other states offer “uninsured motorist physical damage” coverage. Maine does not.

What is Uninsured Motorist Coverage (UM)?

In Maine, Uninsured Motorist coverage is bodily injury coverage only. It protects you and the people in your vehicle by acting as if the person who hit you had the same liability limits you have. UM limits always match your policy’s liability limits. That’s another reason we say don’t cheap out when you choose your liability insurance limit.

Let’s say you’re driving in Portland, Maine. You have Uninsured Motorist coverage with Maine state minimum liability limits of $50/$100. Someone runs a red light and broadsides you. Your daughter goes to the hospital with broken bones and internal injuries. You were not injured as badly. After an ambulance ride, the hospital releases you with minor injuries. Your daughter’s medical expenses are $75,000, and yours are $2,500. In this scenario, you would have to pay $25,000 of your daughter’s medical bills ($75,000 – $50,000) out of pocket. If you had chosen a $300,000 combined single limit, all medical expenses would have been covered 100%.

What is Underinsured Motorist Coverage (UIM)?

Underinsured motorist coverage applies when someone has insurance, but not enough to pay for your injuries. Like Uninsured Motorist coverage, it pretends that the person who hit you had the same limits as you do.

Let’s assume the same accident scenario as above, except the at-fault driver did have insurance with Maine minimum limits of $50/$100. Their insurance wouldn’t be sufficient to pay for your daughter’s medical bills.

If you also had $50/$100 limits, you would still be out of luck. You didn’t buy any more insurance than the person who hit you did. But, if you had chosen a $300,000 limit, your UIM coverage would pay up to $250,000 per person, the difference between your insurance limit and theirs.

Danger: Uninsured Drivers in Vacationland

Although most Maine drivers are insured, remember that tourism is Maine’s largest industry. Visitors from other states are constantly driving among us. They’re in unfamiliar territory, and distracted by Maine’s natural beauty. They’re trying to follow GPS directions. Perfect scenario for an accident, right? Depending on the state they’re from, there’s almost a 25% chance that they have no insurance. So, pay attention to your Uninsured / Underinsured Motorist coverage limit.

What Liability and Uninsured / Underinsured Motorist Limit Should You Choose?

Everyone’s situation is unique. We recommend discussing your situation with a Trusted Choice Independent Insurance Agent. If you live in Greater Portland, contact a Noyes Hall & Allen agent at 207-799-5541 for a custom review of your insurance and your options. We represent most of Maine’s preferred insurance companies, and can help you choose the one that best meets your needs.