Running your small Portland, ME business can be a rewarding and satisfying endeavor. However, without the right liability insurance coverage, running your small business open you up to lawsuits. Here is a brief description from Noyes Hall & Allen Insurance of the most common business liability insurance.

Worker’s Comp

Worker’s compensation insurance is required in Maine for any business with employees. As a business owner, you need to stay up to date on your state’s requirements concerning worker’s compensation insurance. Worker’s compensation insurance protects your employees when they are injured on the job. This also protects you as the employer from liability for said injuries.

Liability Insurance

General liability is one of the most important types of insurance for the small business owner to have. Liability can come in many forms. Individuals can get injured on your property or by your product. Something could go wrong with a service you provided resulting in damage or injury. Liability insurance will protect you in these situations and ensure that your company is not required to pay out of pocket for these types of liability claims.

Commercial Auto

If your company owns vehicles in order to provide services or deliveries, then you need business auto insurance. Commercial vehicle insurance can cover your drivers and your vehicles in the event of an accident. If your company uses vehicles, then you will no doubt have invested a good deal of money into those vehicles. This will protect that investment.

Umbrella Insurance

Commercial umbrella insurance policies help small business cover all their bases in one simple policy. Umbrella policies provide high limits of liabilty over your general liability and business auto policies. To learn more about small businesses, contact our friendly staff at Noyes Hall & Allen Insurance serving Portland, ME at 207-799-5541. We offer a choice of Maine’s best business insurance companies, so we can help you find the best value. We’re independent and committed to you.

Are you a small business owner in Portland, ME looking to protect your assets? The last thing that you need is for disaster to strike and to learn that your policy limits are too low for you to rebuild the company. Noyes Hall & Allen Insurance in South Portland can help you determine how much coverage your small business needs to survive a catastrophic event.

What is considered a small business in Maine?

By definition, a small business owner in Portland, ME is a someone who owns a company with fewer than 50 employees. Technically, sole proprietors are considered small business owners even though they are the only employee at their company. Even those who work from home should consider commercial insurance since homeowner’s policies tend to reject claims resulting from conducting business in the residence. Imagine the entire cost of medical bills for one of your clients resting on your shoulders because your homeowner’s insurance policy refused to cover a business-related slip-and-fall incident!

How much coverage do you need?

The amount of coverage varies by business. Many low-risk companies such as those primarily operated online may think they only need a minimal amount. Retail business owners might understand the exposure to loss that their customers’ foot traffic creates, and be more likely to want higher insurance limits. In reality, your liability limit should be at least $1,000,000 per occurrence – higher if your business’ net worth exceeds that. Of course, Maine small business owners with employees also need to buy workers compensation insurance.

You have worked hard to establish yourself as the owner of your company. Do not let an incident threaten your financial stability. Contact Noyes Hall & Allen Insurance today at 207-799-5541 for a Maine business insurance quote!

If you’re planning to retire or recently retired, CONGRATULATIONS! It’s time to enjoy what you’ve worked so hard for. Many people dream of retiring in Maine. Of course, some of us are lucky enough to already live here!

Retirement finances can be a source of anxiety. No matter how much you’ve saved for retirement, you may wonder:

Will I Outlive My Money?

How Can I Safely Reduce My Monthly Expenses?

Can I Reduce My Insurance Now that I’m Retired?

Can I Live on My Monthly Retirement Income?

Maine Retirees Are:

House Rich – Maine condo and home values are at an all-time high. With even modest savings, you may have a lot of net worth to protect. Make sure you have enough insurance to rebuild or relocate after a disaster. Protect your assets against lawsuits from injuries or property damage you might cause.

Income Tight – You’re on a fixed income. Every monthly payment reduces your retirement fund. You watch expenses more closely than ever.

Closer to Home? – Travel is now for pleasure, not work. You may drive fewer miles than you used to. Do you plan go south in the winter? What happens to your home and your car while you’re away?

Uncertain About the Future – will you stay healthy enough to do the things you want to? If there’s a disaster, will you have enough money to live the life you do now? If you can’t drive, who will help you with your errands?

Done with Property Maintenance – you spent years mowing, shoveling, landscaping and painting. Now someone else can climb the ladder or wrestle the snowblower. Hiring contractors can open you up to liability if they hurt someone – or themselves.

Do You Need Less Insurance in Retirement?

As you prepare for retirement in Maine, you may be eager to reduce your insurance costs. You want to keep monthly expenses down because you’re on a limited income. But you also want to protect the assets you’ve spent your life accumulating. A good insurance agent can help you pick the coverage you need within your budget.

5 Retirement Planning Insurance Value Tips

Buy enough liability insurance – and not too much.

Your auto and homeowners liability insurance limits should at least equal your net worth. If your total assets exceed $500,000, keep your umbrella policy (or buy one). Umbrella policies are one of the best insurance buys; $1 million coverage often costs less than $200 a year.

Watch Your Maximum Out of Pocket

How much are you comfortable paying if something bad happens? Choose your home and auto insurance deductibles with that in mind. Larger deductibles reduce your monthly insurance costs.

Compare Insurance Prices

Because you’ll drive differently, and won’t be working any longer, your underwriting profile changes. Your current insurance company may still be the best value. Or maybe not. A Maine independent insurance agency like Noyes Hall & Allen can compare prices and coverage among several insurance companies with one phone call.

Keep Maintaining Your Property

Regular maintenance helps you budget your expenses and maximize your insurance options real estate value. If you want to change insurers, your new insurance company will inspect your home. Even if you don’t change companies, your insurer may inspect from time to time. If they find something that they’re concerned about, they will require you to repair it. It’s better to keep up with repairs and maintenance on your own timetable.

Choose Contractors Wisely

Hire reputable and trustworthy people to work in and on your property. Ask them for proof of insurance. If they hurt someone or damage their property, or injure themselves, they should be responsible – not you. When hiring cleaning people, home health care or similar service providers, ask if they are bonded. Bonding protects you against theft by someone you’ve let into your home.

Want a Pre-Retirement Insurance Review?

If you’re thinking about retirement in southern Maine, call a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. Or, get several insurance quotes online from our website. We can help you check your current insurance, and let you know if it’s the best value. We can also give you cost-effective advice to customize your insurance to your exciting new life. If you’re moving to Maine in retirement, and looking for a new insurance agent, we’re happy to help. We offer a choice of several of Maine’s top insurers and can do the comparing for you. We can even introduce you to some wonderful local realtors and financial planners.

Either way, you’ll know that your insurance is solid and the cost is reasonable as you head into retirement. At Noyes Hall & Allen, we’re independent and committed to you.

You’ve found your dream home on the coast of Maine. Congratulations! Now you want to protect your investment. And, if you have a mortgage, your lender requires insurance.

Many U.S. insurers restrict coverage for homes and properties near the ocean. They aren’t concerned about storm surge or water damage. Homeowners policies don’t cover flood or surface water. Wind is the issue. Homeowners, condo and renters insurance policies DO cover wind damage. That’s what insurance companies worry about.

The coast of Maine gets few hurricanes or tropical storms. But we still get nasty windstorms. Not as much as warmer states, but often enough. In the past 6 months, southern Maine has had 3 storms with damaging coastal winds. Properties closest to the coast are more susceptible. The same scenic view that drew you to your neighborhood exposes your home to wind. There’s no barrier to break up winds that come off the ocean. Buildings, trees and hills disperse winds farther inland.

Can You Find Insurance on Maine Oceanfront Property?

The good news is that insurance is readily available. Your policy may have a special wind deductible, and you may pay more than your inland neighbors. But you also paid more for your property because of its beautiful location. Higher taxes, too. It’s a lifestyle choice.

How Close to the Coast is an Insurance Problem?

Insurance company underwriting varies. Some insurers will insure any home that’s more than 1000 feet (about 0.2 miles) from the ocean. Others draw the line at 1500 feet. Some apply special wind deductibles for any home within a mile of the coast. Others don’t.

Is this your primary home or a vacation home? Insurers are more eager if they have a chance to write your auto, boat or other insurance.

Is this an island property? Even if your home is more than 1000 feet from the coast, you may have few options available. A knowledgeable local agent can help you find your options.

How To Compare Insurance Quotes for Maine Oceanfront Property

The easiest way to survey the market is to contact an independent insurance agent like Noyes Hall & Allen in South Portland. Unlike State Farm, Allstate, GEICO, Progressive or USAA, we offer a choice of insurance companies. We know Greater Portland and the Casco Bay area. We know which insurance companies will insure coastal properties. We can check the market for the best value combination of price and coverage.

Flood damage isn’t covered by home insurance. The National Flood Insurance Program (NFIP) is a government program insuring against the peril of flood and surface water. Buy it where you buy your home insurance. Every insurance agent can sells it, and the rates are the same wherever you buy it.

Innovative Maine businesses use drones to literally get a new perspective on their operations. Land owners survey lots and buildings. Engineers use photos from unmanned aerial vehicles (UAVs) in project work. Photographers and videographers use drones to capture unique images and videos. Marketers use or hire them to create compelling and disruptive visual content. Even individual hobby fliers own drones now.

Drones: A Money Saving Investment

High quality drones and UAVs are not cheap. It’s easy to invest $15,000 or more in a good quality industrial setup, including cameras and software. Still, that can be a lot less expensive than renting an airplane or helicopter, and offers much more control and flexibility. It’s also safer than sending an employee up on a ladder or bucket to inspect facilities at height. The price of hobby drones has dropped a lot in the last few years. You can find them for less than $1500.

Legal Issues for Drones in Maine

The FAA requires registration of drones and UAVs weighing more than 0.55 lbs. The maximum weight permitted is 55 lbs. Permitted location and other rules vary between pleasure and business use. A remote pilot airman certificate is required as well.

Drone owners and operators face many of the same liability issues as other aircraft pilots. The low altitude operation of UAVs can also create privacy and property issues. Some examples:

Injuring someone, either directly, or by causing an auto accident

Damaging property by striking it

Invasion of privacy or trespass

Even if a claim against you is not valid, defending yourself can cost many thousands of dollars in legal fees in Maine.

Drones are NOT Covered by Standard Insurance Policies

Up to now, few insurers have offered insurance on drones. One of our company partners, Acadia Insurance recently introduced a liability insurance plan for businesses that use drones as an incidental part of their ordinary operations.

If you or your Maine business uses a drone or other UAV, contact a Noyes Hall & Allen Insurance agent in South Portland at 207.799.5541. We’d love to hear how you’re using this innovative technology for fun or business. We can help you manage your risk. We’re independent and committed to you.

If we recommend an insurance company you haven’t heard of, it’s natural to ask how good they are. Noyes Hall & Allen represents many insurance companies. Some are more well-known than others.

Because our companies sell through independent agencies, they advertise very little. By contrast, Geico, Allstate and State Farm advertise nationally to create brand awareness. Geico alone spends $1 BILLION on advertising – about 1 out of every 6 insurance advertising dollars in the U.S.

Good rates are important, but that’s only one reason for choosing an insurance company. Will they pay your claims? Are they easy to work with? At Noyes Hall & Allen, we’ve curated a group of insurance companies that we can stand behind. We work closely with them on behalf of our clients.

How to Choose a Good Insurance Company

There are three important considerations when you evaluate a potential insurer:

Financial solvency – Can the insurance company can pay claims, even in a disaster? Fortunately, A.M. Best studies insurance companies and rates each one for you. Noyes Hall & Allen only chooses insurers rated “A-” (Excellent) or better.

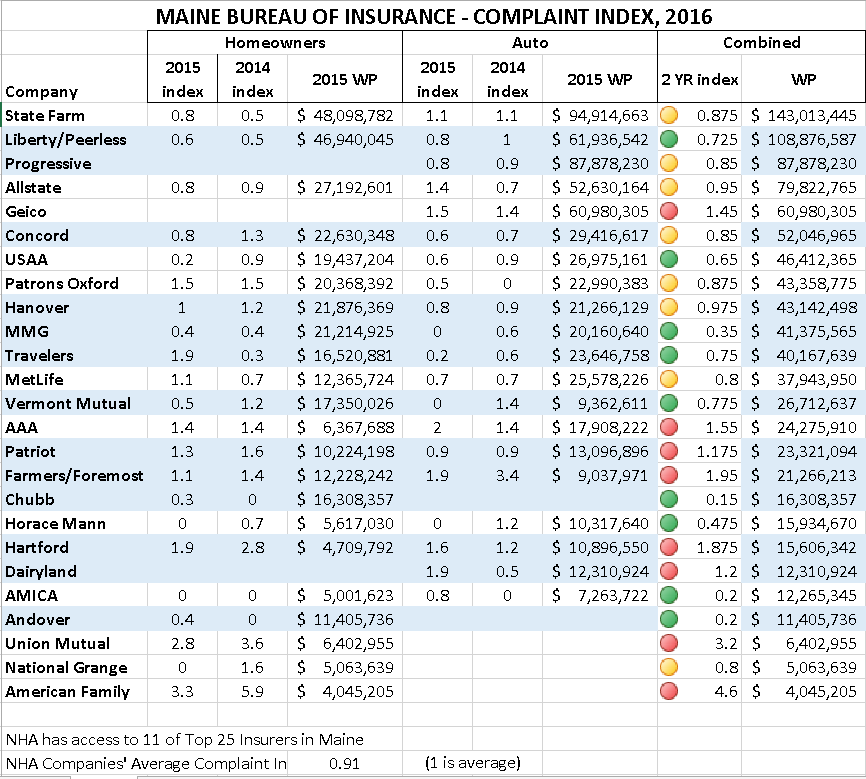

Customer Satisfaction – Feedback from other customers is helpful when evaluating a new insurer. Any company can have complaints; but those with repeatedly good reviews are a better bet to provide good service to you. The J.D. Power national claims satisfaction survey compiles consumer claim feedback every year. But they focus on big national insurers. That excludes many regional insurance companies, which are so important in the Maine market.The Maine Bureau of Insurance indexes home and auto complaints by insurer. It includes Maine’s most important insurance companies. The drawback: the Bureau doesn’t get many complaints each year. That small sample can skew results. The Bureau weighs the ratio of complaints against each insurer to that company’s volume. This weighting levels the playing field. An insurer with an index below 1.00 is “better than average”. Anything above 1.00 is “worse than average”. We’ve included a chart with a recap of those scores below.

Fit with Your Situation – If you insure your beach house with an insurance company that has great financials and terrific reviews, but that company doesn’t like property close to the coast, it’s not going to end well. Some insurers specialize. Others are generalists. Some are comfortable insuring rental properties, or snowmobiles. Others focus on high risk drivers.

Complaint Index – 2016 – Maine Home and Auto Insurance

We compiled this table from data published by the Maine Bureau of Insurance. It shows the 2 year average of home and auto complaint indexes for the top 25 homeowners and auto insurance companies in Maine (by volume). We assigned a “green light” to the companies with ratings in the top 33%, yellow to the middle 33%, and red to the bottom third. Remember, customer satisfaction is only one way to evaluate an insurance company. The companies with the highest satisfaction may not write the kind of insurance you need.

source: Maine Bureau of Insurance. Compiled by Noyes Hall & Allen Insurance

How to Get Quotes from Many Insurance Companies at Once

Noyes Hall & Allen has access to the companies shaded in blue. That’s 11 out of 25, covering more than 50% of the volume in this list. The insurance companies we represent have a complaint index of 0.91 – much lower than the 1.00 average. By the way, insurance agencies have online reviews, too. We’re proud to show the reviews that our clients have left for our agency.

When you contact a Noyes Hall & Allen agent, you’re checking 11 companies at once, backed by our knowledge of where each company excels. Your agent can customize advice to your situation, proposing a solution built just for you.

Many financial advisors recommend personal umbrella coverage to protect your net worth and future earnings. The maximum liability limit offered by most home and auto insurers is $500,000. Even those with modest incomes can exceed $500,000 in net worth, as they pay off debt, accumulate retirement savings, or receive an inheritance.

Maine’s Wrongful Death Statute allows lawsuits up to $500,000 in addition to specific medical or property damages (update: as of 2023, Maine’s Wrongful Death Statute permits up to $1 million in damages, with automatic increases for inflation – even more reason to have an umbrella!) .

If you don’t have enough liability insurance, you could be forced to pay out of your own assets and future earnings. Also, when your insurance runs out, so does your coverage for legal costs.

What Is an Umbrella Policy?

Maine Personal Umbrella Insurance provides excess liability protection above your home, auto, boat, RV and other primary insurance. Umbrella policies are purchased in increments of $1 million. They may be added to a personal package policy or purchased separately on a “stand-alone” policy.

How Much Does Personal Umbrella Insurance Cost?

Maine Personal Umbrella policies are quite inexpensive – often less than $200 per year for $1 million in protection. Insurance companies can offer these low prices because they require you to maintain a certain amount of “underlying” coverage, usually $300,000 or $500,000. Insurers know that claims larger than that are rare, so umbrella policies are priced accordingly.

Can Someone Garnish My Wages?

Absolutely. If you don’t have enough assets to pay for a legal judgement, but you expect to work in the future, the court can garnish a percentage of every paycheck you receive until the debt is paid.

Could I Lose My Home or My Retirement Savings?

Courts don’t like to force someone to sell their primary residence to pay for legal judgement, but it does happen.

How Much Personal Umbrella Insurance Should I Buy?

Umbrella policies come in increments of $1 million. Many insurance companies sell up to $3 million, which is sufficient for many Americans. Higher limits are available, however, for those who need extra protection.

For more information about personal umbrella insurance in Maine, contact Noyes Hall & Allen at 207-799-5541. We would be happy to help you decide if an umbrella policy is right for you.

Rideshare service Uber began operating in Portland Maine at noon on October 2. Uber and its top competitor Lyft are innovative, efficient, popular – and controversial. Everywhere Uber and Lyft pop up, local lawmakers scramble to address it. Taxi operators and other livery drivers rail against it. And insurance companies caution drivers who might think about joining the Uber fleet.

Are Uber Drivers Insured?

If they have a personal auto policy, their own insurance will not cover them while they’re driving someone for a fee. Period. Every PAP excludes coverage while a vehicle is being used as a “public livery or conveyance“, which basically means driving others for hire. An Uber driver in an accident shouldn’t count on their personal insurance helping out.

You can’t blame insurance companies for that. If you’re driving for Uber, you’re probably driving more miles and hours than you otherwise would. You might be in areas unfamiliar to you, under time constraints, and at hours with higher congestion or impaired operators on the road. All of those increase the likelihood you could have an accident.

The Good News Uber’s web site says that the service provides a commercial insurance policy with a $1 million limit per incident, including uninsured/underinsured motorist coverage. That’s more than 90% of drivers in Maine have. It also provides $50,000 of “contingent comprehensive and collision insurance”, which should pay for repairs to an Uber driver’s vehicle as a result of an accident during an Uber trip.

Not So Good News Uber’s insurance drops to to $50,000 per person for bodily injury and $25,000 for property damage “between trips” – the absolute minimum limits allowed in Maine. That’s inadequate for most people who want to protect their assets or future earnings from an expensive lawsuit.

Uber says that most auto insurance policies will provide coverage during the time that the driver is logged on available for hire but between trips. Talk is cheap. Don’t count on an insurance company seeing it the same way. When presented with a claim, expect an insurance company to say you were engaged in livery, just not actively driving someone – and deny your claim.

What Kind of Insurance Should an Uber Driver Have? The only type guaranteed to cover you is a business auto policy, rated as livery use. If you insure your car with Maine commercial vehicle insurance and are upfront about your Uber driving, you should be covered.

Is Uber Rideshare Service Safe to Use?

If you’re thinking of taking a ride from Uber, you can expect that the driver has insurance while you’re in the vehicle. That includes if you’re hit by someone with no insurance. If you have a personal auto policy, you also have Medical Payments coverage (usually $5,000 or less) for minor medical expenses.

Almost every state in the U.S. requires drivers to have car insurance. Like every other law, there are always some people who choose to ignore or disobey it.

The good news: if you are in a crash in Maine, the other driver probably has insurance. Maine is in the Top 10 states for percentage of insured drivers.

The bad news: many Maine drivers carry very low liability limits – as low as $50,000 per person. After an accident, your medical expenses can easily exceed that.

What if the Other Driver Doesn’t Have Enough Insurance to Pay My Damages?

It’s great if the at-fault driver has insurance. Do they have enough insurance to pay your damages? Who knows? At 50/100/25, Maine’s minimum auto liability insurance limits are among the highest in the country. But if you drive a late-model car, $25,000 isn’t going to replace it. If you are badly injured, you can accumulate $50,000 in medical bills in one day. You need to protect yourself.

What Happens if Someone Hits Me and They Don’t Have Insurance?

If an uninsured driver hits you, you have to rely on your own Maine auto insurance. Your collision coverage (if you purchased that option) will pay to repair your vehicle. If you don’t carry collision insurance, you’ll have to deal with the damages on your own. Some other states offer “uninsured motorist physical damage” coverage. Maine does not.

What is Uninsured Motorist Coverage (UM)?

In Maine, Uninsured Motorist coverage is bodily injury coverage only. It protects you and the people in your vehicle by acting as if the person who hit you had the same liability limits you have. UM limits always match your policy’s liability limits. That’s another reason we say don’t cheap out when you choose your liability insurance limit.

Let’s say you’re driving in Portland, Maine. You have Uninsured Motorist coverage with Maine state minimum liability limits of $50/$100. Someone runs a red light and broadsides you. Your daughter goes to the hospital with broken bones and internal injuries. You were not injured as badly. After an ambulance ride, the hospital releases you with minor injuries. Your daughter’s medical expenses are $75,000, and yours are $2,500. In this scenario, you would have to pay $25,000 of your daughter’s medical bills ($75,000 – $50,000) out of pocket. If you had chosen a $300,000 combined single limit, all medical expenses would have been covered 100%.

What is Underinsured Motorist Coverage (UIM)?

Underinsured motorist coverage applies when someone has insurance, but not enough to pay for your injuries. Like Uninsured Motorist coverage, it pretends that the person who hit you had the same limits as you do.

Let’s assume the same accident scenario as above, except the at-fault driver did have insurance with Maine minimum limits of $50/$100. Their insurance wouldn’t be sufficient to pay for your daughter’s medical bills.

If you also had $50/$100 limits, you would still be out of luck. You didn’t buy any more insurance than the person who hit you did. But, if you had chosen a $300,000 limit, your UIM coverage would pay up to $250,000 per person, the difference between your insurance limit and theirs.

Danger: Uninsured Drivers in Vacationland

Although most Maine drivers are insured, remember that tourism is Maine’s largest industry. Visitors from other states are constantly driving among us. They’re in unfamiliar territory, and distracted by Maine’s natural beauty. They’re trying to follow GPS directions. Perfect scenario for an accident, right? Depending on the state they’re from, there’s almost a 25% chance that they have no insurance. So, pay attention to your Uninsured / Underinsured Motorist coverage limit.

What Liability and Uninsured / Underinsured Motorist Limit Should You Choose?

Everyone’s situation is unique. We recommend discussing your situation with a Trusted Choice Independent Insurance Agent. If you live in Greater Portland, contact a Noyes Hall & Allen agent at 207-799-5541 for a custom review of your insurance and your options. We represent most of Maine’s preferred insurance companies, and can help you choose the one that best meets your needs.

Many people buy insurance one policy at a time, as the need arises. It makes sense: you buy a car, then rent an apartment, then buy a condo or home, and maybe a boat or other toy later. Maybe you bought one online, another over the phone, and the third from an agent.

It’s easy to keep the policies you’ve always had. But smart insurance buyers know that it makes sense to combine their insurance with one company (some people call it “bundling insurance”). And, the smartest ones know to use a Maine Trusted Choice independent insurance agent.

10 Reasons Why Smart People Combine Home and Auto Insurance

1) Saves Time – Who wants to figure out which company insures what, make 3 different phone calls, remember multiple passwords, or enter duplicate info online, when they can do it once?

2) Higher liability protection- Most insurers will only provide their highest liability protection (personal umbrella insurance) if they insure at least your home & auto.

4) Less Likely to Miss Something Important – Let’s say you move; you might remember to change your home insurance, but forget to change the address on your auto or boat policy. Next thing you know, your other policy is canceled because you didn’t get a bill.

5) Big Love (or at least respect) from the Insurance Company – All businesses value you more when you do more business with them. In the insurance world, that can come in handy if you ever need a favor (e.g. you missed a payment while you were on vacation, or need to insure something unusual).

6) Your Agent Knows You Better – The more your agent knows you, the better advice they can provide, and the more effectively they can advocate for you. Wait, you DID buy insurance from a human – not a reptile or a computer – didn’t you?

7) Save Money – Most insurers save their best pricing for customers with more than one policy. If you’re only buying one policy from them, you can do better.

8) Easier to Insure the Risky Stuff – Insurers aren’t lining up to sell you fire insurance for your remote getaway camp. But, if it’s just another part of your portfolio of coverage with that company, they’re much more likely to accommodate you.

9) Better Coverage – Some insurers offer special coverage forms only available to clients who “bundle” auto & home insurance.

10) Perks – One example: Hanover Insurance’s Platinum Experience (link to .pdf) is only available to package customers. It features perks like home inventory tools, exclusive claim contacts, and auto repair diagnostics and estimates.

Maine Retirees Are:

Maine Retirees Are: