The secret is out: Portland, Maine is a great place to live. Friendly neighbors, excellent restaurants, and safety make it a popular choice for families and retirees.

Even in a safe place like Maine, bad things can happen. If you have to file a home insurance claim you want to be confident that your insurance policy will help get life back to normal. When it comes to home insurance, you want to know that your agent is on your side. The team at Noyes Hall & Allen Insurance has been committed to you since 1933.

How Does a Home Inventory Help Me?

When you file a home insurance claim, your insurance company needs to know what you lost. Then they pay you to replace it. Imagine after a tragedy trying to remember everything you had in your home, every drawer and cabinet. It’s overwhelming.

You can avoid stress and frustration by preparing a home inventory. This creates a record of all the rooms in your home and what was in them. You can do it with a video walkthrough of your home, computer spreadsheet or even on paper. Either way, aim for as much backup information as possible, and update periodically. Recording details like model numbers and receipts are a good start. Store the inventory in a safe place, and back it up in the cloud or in your safe deposit box.

We are independent agents. That means we offer you lots of choices from a wide variety of insurance companies. We will help you find the best value for the coverage you need. We’re independent and committed to you.

Conditional renewal occurs when your insurance company makes changes to your policy that you did not request. These changes can range from minor adjustments to significant alterations. It’s essential to understand what these changes mean for you..

When Do Insurers Use Conditional Renewal?

Insurance companies often change underwriting requirements. They often “grandfather” in-force policies from these changes. But sometimes conditions change dramatically. Then the insurance company decides to make wholesale changes, even to in-force policies. Or, the insurance company may take a specific action on your policy.

Common Conditional Renewal Types

These are the most common changes in a conditional renewal:

Deductible changes – This could mean an increased deductible or the introduction of a new type, such as a separate wind or hurricane deductible.

Liability Limits – Your liability insurance protection might be reduced, for example, from $500,000 to $100,000.

Coverage exclusions or reductions – Certain coverages, like towing or roadside assistance, might be removed or reduced.

Large rate increases – Some states require notification of significant price increases, though this is not the case in Maine.

Why Am I Getting a Conditional Renewal?

Your insurer might be implementing an across-the-board change, such as a new minimum deductible or a wind deductible for any property in a certain location.

Or the underwriter could be taking specific action on your policy. This is usually in response to claims or some condition that they’ve identified. In this kind of conditional renewal the notice will list the reasons.

Is the Insurance Company Canceling My Policy?

No, a conditional renewal is NOT a non-renewal. The insurance company is offering to renew your policy, however with different terms than before. On the other hand, if the insurance company mails you a Notice of Nonrenewal, they are terminating your contract.

Do I Have Options?

You’re not required to accept the conditional renewal, but it might still be the best deal for you. Conditional renewal is often a re-calibration to the market. In other words, your insurance company is doing what most new insurers would do.

However, you can check with your Noyes Hall & Allen agent to see what they think. We offer a choice of several insurance companies. That gives us good perspective on the market so that we can provide personal advice for your specific situation. We like to say we’re independent and committed to you.

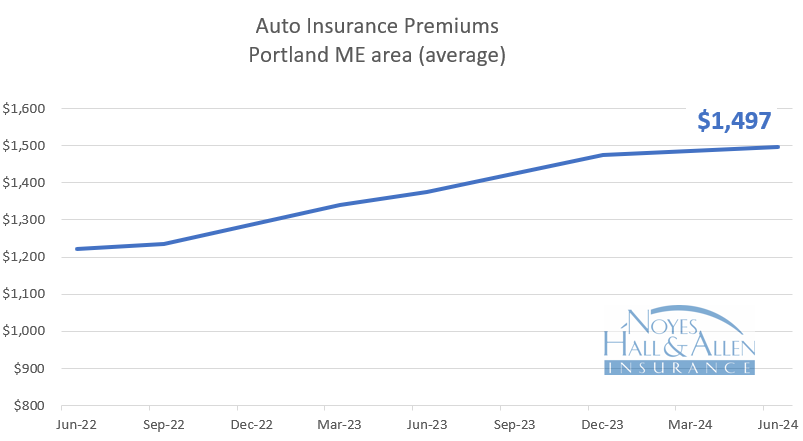

Maine home and auto insurance rates are rising faster than the national average in 2024. Although Maine rates are still among the lowest in the USA, Portland Maine area insurance buyers saw almost a 15% price increase in the first half of 2024. Industry experts expect this to continue through 2024, with some optimism that the increases will be less next year.

Maine Auto Insurance Rates – June 2024

Portland Maine auto insurance rates jumped 13.0% on average in the 2nd quarter of 2024. The average annual auto insurance policy in Cumberland County now costs $1497 per year. Rates vary depending on the type and number of vehicles, drivers and other factors.

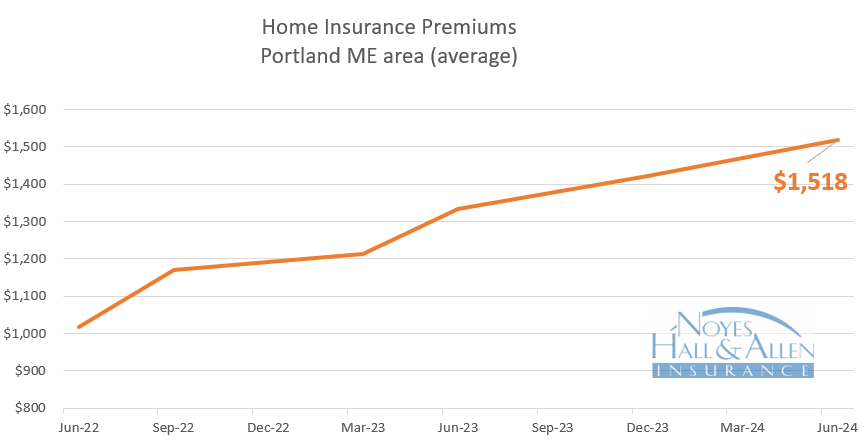

Maine home insurance rates continue to increase even faster than auto insurance. The average home insurance premium was 13.7% higher than a year ago. The end is not in sight yet, as US home insurers report record losses from weather events.

Fortunately, historically high rebuilding costs have tempered somewhat. This allowed insurance companies to reduce their “inflation guard” factors. That reduces the percentage increase, which was about 4 percentage points lower than our last survey in December.

Independent Agents Offer a Choice of Maine Home and Auto Insurance Rates

For more than 90 years, Noyes Hall & Allen has helped southern Mainers navigate the insurance market. While we don’t have any control over prices, we offer a choice of several insurance companies. That means we can help you find the best insurance value in any market.

Rate Increases, Cancellations and Coverage Reductions – What You Can Do About It

It’s clear that Maine property insurance is facing challenges in 2024. Homeowners are feeling the impact. Rising rates, policy cancellations and coverage cutbacks are common. It’s not just a coastal problem. People all over Maine are discovering that insurance underwriters hold the cards in this market. How and why is the insurance market so hard right now? Do you have any recourse? What can you do to control costs?

What’s Going on in the Maine Property Insurance Market?

Why Property Insurance is So Painful in 2024

There are many reasons, but they all come down to cost. Insurance is designed to share costs and spread risk. Claims of the few are paid by the many through insurance premiums. Insurance companies are well-funded. They have reserves to pay out more than they collect in premiums for a short time. But those costs are then passed on. Otherwise, the system falls apart and everyone loses.

Insurance claim costs have spiked in many areas for various reasons. They include:

Inflation in materials – Rising costs for building materials, auto parts, and medical supplies contribute to higher claim expenses.

Increased claim severity – More frequent and severe weather events, changes in property use, and an increased number of seasonal and secondary properties lead to larger claims.

Longer repair times – Shortages in parts, materials, and labor result in extended repair durations, impacting expenses for auto rentals, temporary housing, and commercial relocation.

Reinsurance costs – Insurance companies buy reinsurance to protect themselves from disasters. Shrinking reinsurance capacity since 2020 has led to price hikes for insurers.

Catastrophes Can – and Do – Happen in Maine

Mainers often think that weather disasters happen “somewhere else”. But they do happen here. And lately they’ve been more frequent.

Verisk defines a catastrophe (“CAT”) as an event resulting in more than $25 million in insured losses. Regional insurers may see an average of 4-5 “CAT” events per year in Northern New England. In 2023 there were 8.

There aren’t just more catastrophes than normal. They’re bigger too. Their 2023 expected payout for damage from CAT claims was nearly 8X an average year. We don’t see signs of improvement right away. 2024 started with a major wind and rainstorm.

Changes in Your Maine Property Insurance

Maine property owners are seeing a lot of changes in their insurance. Most of it is not good news. Here are some things you might experience:

Increasing rates – Even homeowners with no claims experience are facing rising rates, with the current average increase around 17% in Maine.

Saying “no” -Moving to a different insurance company during this time can be risky, as many insurers decline to quote on properties they consider higher risk.

Tougher inspections – Insurers are inspecting properties more often and more closely. They’re focusing on roof condition and overhanging trees. Some are even using aerial photographs to spot hazards.

Bumping deductibles – Many coastal properties now have big wind deductibles. Some insurers are increasing deductibles across the board. Others are only increasing deductibles if you’ve had several claims.

Mandatory alarms – Insurers require owners of high value or secondary homes to install central alarm systems to warn against water leakage, low temperature, fire and burglary.

Required increases in insurance amount – Building material and labor cost increases mean higher costs to rebuild your home. Insurers review that cost periodically and require you to insure to the full rebuilding cost. (Although it costs more, it’s important to make sure you have enough insurance to rebuild – this is a benefit).

Cancellation or non-renewal – Insurers may cancel policies due to claims or if homeowners fail to make necessary improvements after an inspection.

Is All of This Legal?

The Maine Bureau of Insurance plays a crucial role in regulating insurance companies offering Maine property insurance. Here are some key points:

Rate Approval and Policy Changes

The Bureau approves rates for insurers authorized to do business in Maine.

They also permit cancellation or non-renewal for certain reasons. Those reasons include failure to comply with reasonable loss control recommendations or failure to permit inspection.

Insurers can make changes to policy terms, which is known as a “conditional renewal.”

If an insurer decides not to renew your policy, they must send you a “legal notice of non-renewal.”

Challenging a Non-Renewal

As a policyholder, you have the right to challenge non-renewal by appealing to the Maine Bureau of Insurance.

However, insurers typically adhere to non-renewal rules, making successful appeals less common.

How to Control Maine Property Insurance Costs

Although you can’t completely avoid large market forces, you can do some things to control your Maine property insurance costs and protect your property.

Pro-actively protect your property – regularly trim trees and shrubs away from buildings. Install a generator or backup sump pump. Keep gutters clean. Use a low-temperature alarm if you’re often away from the property.

Keep up on maintenance – take care of peeling paint or moss or debris on your roof. Replace roof shingles before you get water damage (hint: like tires, shingles don’t usually last as long as the warranty may say).

Stay claim-free – Small insurance claims sit on your record for 5 years or more. Many insurance companies decline to insure new properties if they have multiple property claims.

Watch your credit score – insurers “score” policies to set rates. An insurance score is closely related to your credit score. The better your score, the lower your rate.

Choose a local insurance agent – Local knowledge can be the difference between getting property insurance and not. National insurers and 800 number agents don’t know your area like a local advocate.

Communicate with your insurance agent. Let them know if you make improvements, install alarms or generators, or pay off your mortgage. All of those might reduce your insurance premium.

Help Navigating Maine Property Insurance

If you own property in Southern Maine, contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We offer a choice of Maine’s top insurance companies. While we don’t control the market, we have a good perspective on current conditions. We can help you find the best fit and value for your property insurance.

Maine insurance rates follow national and local trends and claim experience. Home and auto rates continue to rise as insurers and customers struggle with rising costs. Portland Maine area insurance buyers saw more than a 15% price increase in 2023. Industry experts expect this to continue in 2024. Still, Maine insurance rates remain among the lowest in the US.

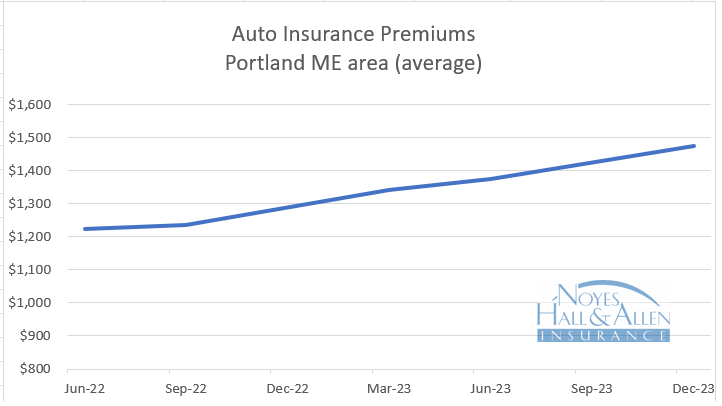

Maine Insurance Rates – December 2023 – Auto

Portland Maine area auto insurance rates jumped 14.4% on average in 2023. The average annual auto insurance policy in Cumberland County now costs $1475 per year.

According to a report by Insurify, personal auto prices were up 17% countrywide in the first half of 2023. The Bureau of Labor Statistics reported that auto insurance prices increased 20.3% in 2023. Maine rates increased even more: 28% statewide, according to Insurify. That was the 6th highest rate in the US.

Several factors put strong upward pressure on auto insurance rates everywhere in the US:

Used auto prices are at an all-time high.

New vehicles have much more technology, which makes parts more expensive to replace.

Auto body shops are backlogged, increasing auto rental costs

Auto parts and labor remain scarce, increasing prices

Medical care inflation is high.

Will auto insurance rates level off in 2024? We don’t see any signs that they will. Neither does the financial advice site Motley Fool.

The good news is that Maine auto insurance rates are the lowest in the US according to the Value Penguin “State of Auto Insurance 2024” report. They report that the average Mainer pays $92 per month for car insurance, 44% less than the national average.

Maine Insurance Rates – December 2023 – Homeowners

Maine home insurance rate increases continue to outpace even large auto insurance increases. The average home insurance premium was 17.7% higher than a year ago. The end is not in sight yet, as US home insurers report record losses from weather events and historically high rebuilding costs.

Many of the same insurance inflationary factors described above affect home insurance. But reinsurance costs remain one of the biggest drivers of property insurance rates. Reinsurance is insurance for insurance companies. It protects them against catastrophic losses from natural disasters like wildfires, blizzards, ice storms, hurricanes and tornadoes. Many insurance companies continue to see their reinsurance costs jump 30-50% this year. Insurance companies pass on that cost to their customers.

Although this isn’t great news for Mainers, we’re better off than many areas of the country. Extreme weather has caused wildfires in the west and north, tornadoes and heat in the south and torrential rains elsewhere. Insurance companies have responded by canceling policies in Florida, Louisiana and California, and reducing their new policy offerings elsewhere.

For more than 80 years, we’ve helped southern Mainers navigate the insurance market. While we don’t have any control over prices, we offer a choice of several insurance companies. That means we can help you find the best insurance value in any market.

A water shutoff system can help avoid a common cause of building damage: water leaks. They aren’t cheap, but neither is water damage. Some insurers offer discount codes for these systems. Installing one may also qualify you for an insurance discount.

Water – The Most Common Property Insurance Claim

Most home and business owners worry about fire or theft damaging their property. But water damage is far more likely. According to Leak Defense, you are 7X more likely to have water damage than a fire. Moreover, water losses are 6X more common than burglaries.

There are 2 broad categories of water damage:

Weather related water damage such as: ice dams; wind-driven rain; or backup of sewers or drains.

Non-weather related water damage such as: plumbing leaks; tub overflows; or frozen pipes.

Water Damage is Expensive and Disruptive

Water damage is expensive. The average 2018 water damage claim for Hanover Insurance was $10,849. That’s just the water damage, not including the insurance deductible or the plumber’s bill to fix a leaky fixture. And costs have only increased since then. This Hanover Insurance infographic shows that buildings older than 20 years are more likely to have issues.

Water damage also disrupts your life or business. Hanover reported that the average length of impact from water damage to homes was 3 to 6 months. In severe cases, that can mean moving out of your home during repairs.

Water Shutoff Valves Can Minimize Losses

A water shutoff system does just what its name suggests. It monitors water flow in a building’s plumbing and automatically shuts off the water when it detects too much. It also alerts the building owner or manager so they can correct the problem.

The longer water flows from a leak, the more damage it causes. Shutting the water off quickly reduces the extent of water damage. That can be the difference between a minor mess and a major disaster.

How Much Do Water Shutoff Systems Cost?

Prices vary from building to building. For example, a professionally installed shutoff device in a home might cost $3,000 to $5,500. Commercial installations would cost more.

Sensor systems without shutoff valves can cost as little as $100 and you can install them yourself. However, low-cost sensors only alert you. They don’t shut off the water, which is so important to reduce damage.

Some insurance companies offer discount codes or special pricing for water shutoff systems. Check with your agent to see if your insurance company does this.

Insurance Discounts for Automatic Water Shutoffs

Many insurance companies offer discounts for customers who install automatic water shutoffs. Although the discount is only a fraction of the cost of the system, it helps offset the cost and rewards those who take this extra step to protect their property.

Not every system qualifies. Most insurers require:

Automatic water shutoff valve

24/7 reporting to a monitored service

an approved vendor. This varies by insurance company. Check with your agent before you commit to install one.

Answers to Your Water Damage Insurance Questions

Do you own a home, condo or business in the Portland Maine area? Contact a Noyes Hall & Allen Insurance agent in South Portland. We offer a choice of Maine’s top personal and business insurance companies. That means we can search and compare for the best value for you.

Personal injury liability coverage fills an important coverage gap in many policies. Off-the-shelf personal and business liability policies cover Bodily Injury and Property Damage. But you can be sued for reasons that fall between the cracks.

Invasion of Privacy – interfering with someone’s right to be left alone or to control their personal space or information.

Libel – writing, posting or publishing something false or damaging about someone.

Slander – saying or broadcasting something false or damaging about someone.

False arrest – detaining someone without legal authority or justification.

Malicious prosecution – bringing legal action against someone with the intent to harm them. Suing someone without reasonable grounds.

This coverage is not included in the standard homeowners, renters, condo or business liability policies. You can usually add it for a small additional premium.

What Are Some Examples of Personal Injury Liability Claims?

A person posts on Instagram about a negative experience at a restaurant. The restaurant owner sues for libel.

A landlord enters an apartment to check something while the tenant isn’t home. The tenant finds out and sues for invasion of privacy.

At happy hour, a golf club member tells others that a certain member cheats. That member sues the accuser for slander.

A homeowner sees someone in the neighborhood who looks suspicious to them. They call the police and detain them until the police arrive. The person is actually a fellow resident out for a walk. They sue the caller for false arrest.

A parent posts photos online of their child’s soccer game. Another parent sues the poster for invasion of privacy.

A store owner accuses teen of shoplifting. They keep them in the store until the police arrive. Even though the police confiscate the stolen items, the teen’s parents sue the store for false arrest.

A resident puts a large sign on their lawn, against HOA rules. Another neighbor complains. The neighbor with the sign sues the other for malicious prosecution.

What Does Personal Injury Liability Insurance Pay For?

If someone sues you for these types of injuries, Personal Injury insurance can:

Provide an attorney to defend you – even if the claim is baseless.

Pay legal fees and court costs

Pay settlements or judgments

Who Needs Personal Injury Coverage?

Almost everyone is exposed to personal injury liability. For example, if you or a family member:

Live, work or go to school near other people

Have a high-profile job or volunteer position

Use social media

Own income property

Encounter someone with a history of disputes with others.

Liability Insurance in Maine

Do you live or own a business in Southern Maine? Looking for answers about liability insurance? Contact a Noyes Hall & Allen Insurance agent in South Portland. We offer a choice of Maine’s top insurance companies. We’ll do our best to help you find the right coverage within your budget.

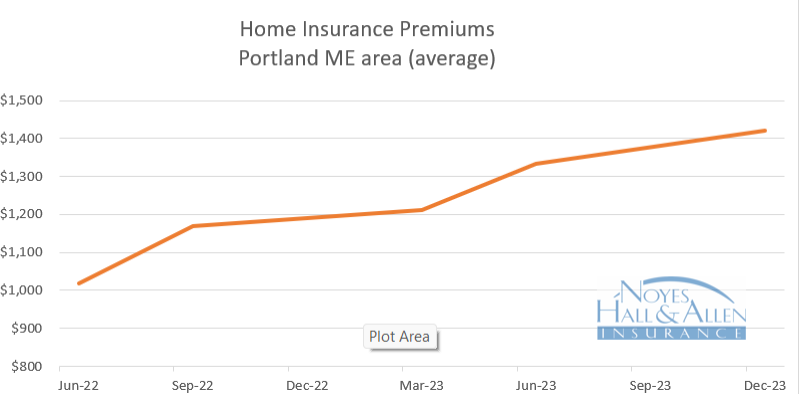

Maine insurance rates are affected by national and local trends. Home and auto rates continue to jump as insurers and customers struggle with rising claim costs and construction values. Portland Maine area insurance buyers saw almost a 15% price increase in the 2nd quarter of 2023. Still, Maine insurance rates remain among the lowest in the US.

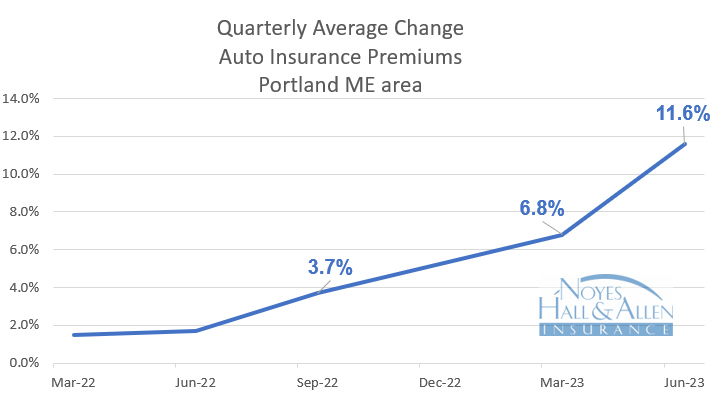

Maine Insurance Rates – April to June 2023 – Auto

In the 2nd quarter of 2023, Portland Maine area auto insurance rates jumped 11.6% on average at renewal, up from 2% a year ago. The average annual auto insurance policy in Cumberland County costs $1374 per year.

According to a report by Insurify, personal auto prices were up 17% countrywide in the first half of 2023. Insurify says that Maine rates increased even more: 28% statewide. That was the 6th highest rate in the US.

Insurers continued to report higher than expected losses as body shops and mechanical repair shops passed along higher costs. Used auto prices spiked during COVID and settled above pre-pandemic levels. Finally, auto rental times remain very long as body shops require much more time to schedule repairs. All of these factors, along with medical cost increases, put strong upward pressure on auto insurance rates in 2Q 2023.

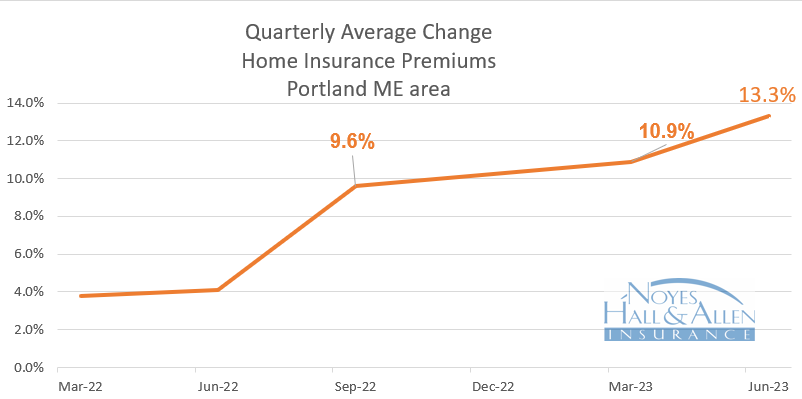

Maine Insurance Rates – Home – April to June 2023

Maine home insurance rate increases continue to outpace even large auto insurance increases. The average home insurance premium was 13.3% higher than a year ago. That’s up from 4% a year ago. The end is not in sight yet.

Many of the same inflationary pressures pushed home prices higher. Building materials and labor costs have dropped from post-COVID peaks, but remain historically high. It’s been difficult and expensive to find contractors. That delays repairs and increases claim costs.

But reinsurance costs remain one of the biggest drivers of property insurance rates. Reinsurance is insurance for insurance companies. It protects them against catastrophic losses from natural disasters like wildfires, blizzards, ice storms, hurricanes and tornadoes. Many insurance companies continue to see their reinsurance costs jump 30-50% this year. Insurance companies must pass on that cost to their customers.

Although this isn’t great news for Mainers, we’re better off than many areas of the country. Extreme weather has caused wildfires in the west and north, tornadoes and heat in the south and torrential rains elsewhere. Insurance companies have responded by canceling policies in Florida, Louisiana and California, and reducing their new policy offerings elsewhere.

Compare Your Options with an Independent Agent

Most financial advisors recommend comparing to get the best insurance value. If you live in southern Maine, you can get up to 5 insurance quotes in 10 minutes from our website. Or contact a Noyes Hall & Allen agent in South Portland at 207-799-5541 for a free no-obligation custom review. We offer a choice of several insurance companies. That means we can help you find the best insurance value.

Off the shelf policies don’t provide proper artwork insurance. Homeowners, renters and condo policies have limited coverage. To really protect your collection requires a bit more.

GOOD – Basic Policies and Artwork Insurance

Home, condo and renters policies protect your belongings. They pay for damage by fire, theft plumbing leaks and 14 other perils. Personal Property (Coverage C) is the most your policy will pay. Off-the-shelf policies value your property at Actual Cash Value. That’s defined as replacement cost minus depreciation. That’s a start, but we recommend more.

BETTER – Two Upgrades for Artwork Insurance

Even if you don’t have much artwork we recommend two important upgrades to the base policy.

Replacement Cost Coverage for Personal Property. You want the insurance company to pay you the full cost to replace damaged or destroyed items. This endorsement removes the depreciation deduction. Only your deductible applies. We sometimes call this “new for old” coverage.

Replacement cost coverage is an option on homeowners, condo or renters policies.

Special Coverage for Personal Property – also called “open perils” or HO-5 coverage. This expands the causes of loss that your policy covers. The basic policy covers 16 named perils. That’s exactly what it sounds like. Only listed perils are covered. Some examples: fire; vandalism; smoke; and plumbing leaks.

But what if you leave your window open, and rain damages your artwork? Or, someone spills wine on it? Those aren’t among the 16 named perils. You need open perils coverage for your policy to pay.

BEST – Scheduled Artwork Insurance

Scheduling your valuable articles gives the best artwork insurance coverage. That means listing and describing each piece and assigning a value to it. This is the best way to insure many types of valuables. That includes jewelry, antiques, rugs or special collections. You may see it on your policy as Scheduled Personal Property.

Important Benefits of Scheduling Artwork

Sets the value BEFORE a loss – it can be hard to describe your artwork after it’s completely destroyed or stolen. It’s also difficult to prove what it was worth. Scheduling it establishes the value before the loss, not after. The insurance company will pay the lesser of

the cost to repair the item;

the cost to replace the item;

the amount listed on the schedule.

Provides Special Coverage – like the open perils coverage described above. For example: hanging hardware fails and a painting crashes to the floor. The frame breaks. It’s covered! But it wouldn’t be without special coverage or scheduling.

Removes the deductible – most property policies have a $1000 deductible or more. But scheduled property is usually covered with no deductible at all.

Valuing Your Artwork for Insurance

Many insurers allow you to set the value of your own artwork up to a limit. Often, that limit is $5,000. Any single piece valued over that needs an appraisal to justify the value. Insurance companies may require updated appraisals every 5 years. They want to make sure the valuation stays current.

If you have a lot of art or other valuables an insurance company might require an alarm system in your home. That usually means a system that’s monitored 24/7 by a service, not self-monitored via app or cell phone.

Want to Insure Your Maine Art Collection?

Do you live in Southern Maine and need artwork insurance? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We offer a choice of Maine’s preferred home insurance companies. We can help you find the best value for your collection.

Maine insurance rates are following national trends. Home and auto rates are up as insurers try to catch up with rising claim costs and construction values. Portland Maine area insurance buyers saw almost a 10% price increase in the 1st quarter of 2023. Even so, Maine insurance rates remain among the lowest in the US.

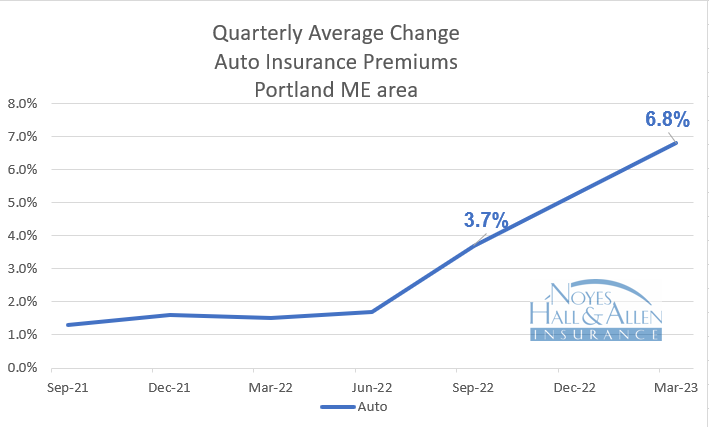

Maine Insurance Rates – Auto – January to March 2023

Between January and March 2023, Portland Maine area auto insurance rates jumped 6.8% on average at renewal, up from 3.7% last September. The average annual auto insurance policy in Cumberland County costs $1341 per year.

Insurers reported higher than expected losses as people drove more after COVID reductions. Body shops and mechanical repair shops charged higher prices due to supply chain and labor shortages. Used auto prices spiked during COVID and settled above pre-pandemic levels. Finally, auto rentals are much more expensive, and needed longer due to body shop delays. All of these factors, along with medical cost increases, put strong upward pressure on auto insurance rates in 1Q 2023.

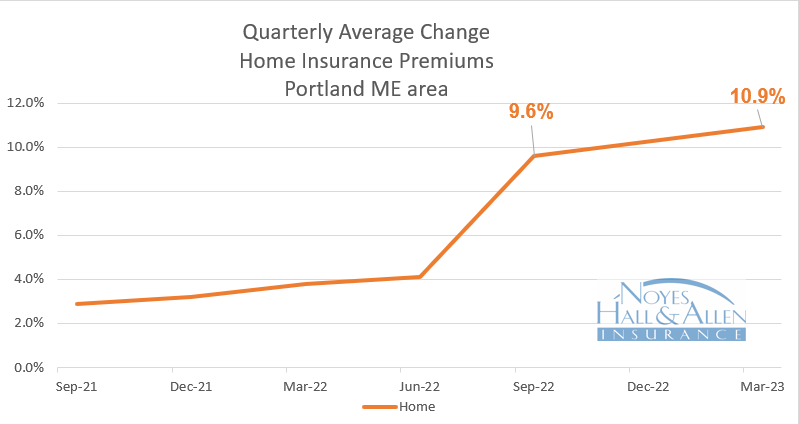

Maine Insurance Rates – Home – January to March 2023

Maine home insurance rates increased even faster than auto insurance. The average home insurance premium was 10.9% higher than a year ago. That’s up from 9.6% in September. And we haven’t seen the end yet.

Many of the same inflationary pressures pushed home prices higher. Building materials and labor costs spiked dramatically during COVID and haven’t settled completely back. It’s been difficult and expensive to find contractors. That delays repairs and increases claim costs.

But reinsurance costs are probably the biggest driver of property insurance rates. Reinsurance is insurance for insurance companies. It protects them against catastrophic losses from natural disasters like wildfires, blizzards, ice storms, hurricanes and tornadoes. Many insurance companies saw their reinsurance rates jump 30-50% this year. Insurance companies must pass on the cost of reinsurance to their customers.

Compare to Find the Best Value

Most financial advisors recommend comparing to get the best insurance value. If you live in southern Maine, you can get up to 5 insurance quotes in 10 minutes from our website. Or contact a Noyes Hall & Allen agent in South Portland at 207-799-5541 for a free no-obligation custom review. We offer a choice of several insurance companies. That means we can help you find the best insurance value.