Running your small Portland, ME business can be a rewarding and satisfying endeavor. However, without the right liability insurance coverage, running your small business open you up to lawsuits. Here is a brief description from Noyes Hall & Allen Insurance of the most common business liability insurance.

Worker’s Comp

Worker’s compensation insurance is required in Maine for any business with employees. As a business owner, you need to stay up to date on your state’s requirements concerning worker’s compensation insurance. Worker’s compensation insurance protects your employees when they are injured on the job. This also protects you as the employer from liability for said injuries.

Liability Insurance

General liability is one of the most important types of insurance for the small business owner to have. Liability can come in many forms. Individuals can get injured on your property or by your product. Something could go wrong with a service you provided resulting in damage or injury. Liability insurance will protect you in these situations and ensure that your company is not required to pay out of pocket for these types of liability claims.

Commercial Auto

If your company owns vehicles in order to provide services or deliveries, then you need business auto insurance. Commercial vehicle insurance can cover your drivers and your vehicles in the event of an accident. If your company uses vehicles, then you will no doubt have invested a good deal of money into those vehicles. This will protect that investment.

Umbrella Insurance

Commercial umbrella insurance policies help small business cover all their bases in one simple policy. Umbrella policies provide high limits of liabilty over your general liability and business auto policies. To learn more about small businesses, contact our friendly staff at Noyes Hall & Allen Insurance serving Portland, ME at 207-799-5541. We offer a choice of Maine’s best business insurance companies, so we can help you find the best value. We’re independent and committed to you.

When the blows hard many homeowners and business owners discover that their insurance policy has a wind deductible. Windstorm insurance deductibles have been common in the Southern US for years. In Maine, they’re more commonly found on insurance policies for coastal or island properties.

Not every insurance policy in Maine has a separate wind deductible. If your policy doesn’t list one, then your regular property deductible applies to wind damage.

Wind Deductible Amounts – Flat or Percentage

Most homeowners and business property policies have a flat deductible that applies to all causes of loss. These are fixed dollar deductibles. For example if your deductible is $1,000 it applies whether you have a break-in, fire, water or wind damage, you pay the first $1,000.

Many wind deductibles are “percentage deductibles“. The deductible is a percentage of the insurance amount, NOT the actual loss. For example, if your home is insured for $500,000 and has a 1% wind deductible, a $5,000 deductible applies to wind damage, and your flat deductible applies to other causes of loss.

Common Types of Windstorm Damage in Maine

Wind blows a tree onto property, damaging it.

Wind damages roof shingles or siding.

Wind-driven rain lifts shingles and siding, allowing water into the building.

Three Types of Wind Deductible in Maine Insurance

Hurricane deductibles

“Named Storm” deductibles

Wind deductibles

Hurricane Insurance Deductible

A hurricane deductible only applies if your wind damage was caused by an actual hurricane. If your property is damaged by wind during any other kind of storm, the deductible doesn’t apply. Insurance policies define when a hurricane deductible applies. Usually it’s during the time and place that a hurricane watch or warning is in effect.

“Named Storm” Insurance Deductible

“Named storms” include tropical storms and depressions, as well as hurricanes. These occur more frequently, so “named storm” insurance deductibles are more likely to be applied. A homeowner would rather have a hurricane deductible.

Historically, “named storms” were limited to tropical cyclones. But in recent years, the National Weather Service has begun naming winter storms. Does wind damage that occurs in one of these named winter storms cause the “named storm deductible” to apply? That’s unclear. In our South Portland Maine insurance agency, we haven’t heard of an insurance company invoking that. But, it could happen.

Wind Damage Insurance Deductible

Wind deductibles apply to all kinds of wind damage, including those caused by hurricanes, named storms, or other wind. Even moderate winds can cause damage to property. A homeowner or business owner would prefer a hurricane deductible or a named storm deductible to a wind deductible. That’s because windy days happen much more frequently than hurricanes.

Which Insurance Companies Use Wind Deductibles?

Some insurers use only hurricane deductibles. Others use Named Storm deductibles. Still more use wind deductibles. And some don’t use wind deductibles at all.

Each insurance company has its own guidelines. Some large national insurers use a wind deductible for any property within 1 or 2 miles of the coast. That’s a lot of homes in Maine. Many use special deductibles for properties within 1000′ of the coast.

The geography of Maine’s coast varies greatly. South of Portland, much of the coast is low-lying beaches open to the Atlantic. This allows ocean windstorms to affect properties farther from the shore. North of Portland, the coast is more rocky and rugged. Many elevated peninsulas create leeward inlets and protected harbors.

Some insurance companies that understand Maine underwrite these coastal areas differently. They may require a special deductible for properties more exposed to wind, and not for others.

Does Your Insurance Policy Have a Wind Deductible?

If your policy has a separate windstorm deductible, contact Noyes Hall & Allen Insurance in South Portland at 207-799-5541. We offer a choice of many of Maine’s preferred home and business insurance companies. Depending on the location of your home, we may find an insurer willing to insure your property with a flat deductible. This could save you thousands of dollars in case of windstorm damage.

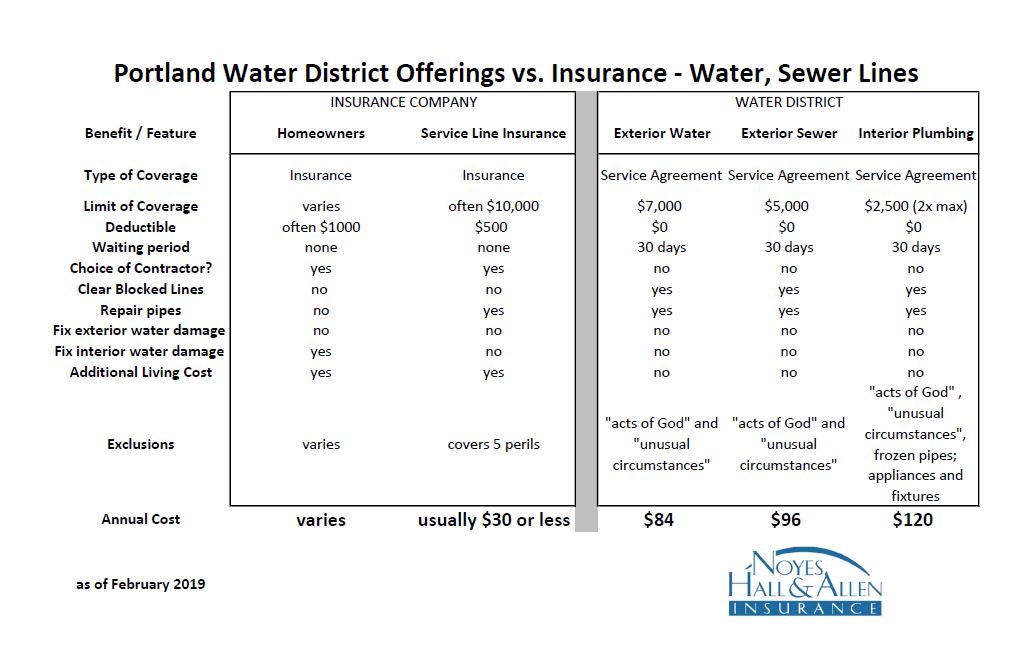

The Portland Maine Water District offers Home Serve service agreement products. There are three options: exterior water lines, exterior sewer lines, and interior plumbing.

Does a water district plan duplicate coverage you already have under your homeowners?

Can you buy water or sewer line coverage from an insurance company?

Is it cheaper to buy water line coverage from an insurance company, or the water district?

We’ve created a spreadsheet comparing what’s covered by the water district plans with what insurance products cover. We’ve also outlined the cost and benefits of each. This 11 minute video reviews it in detail:

If you prefer to look at the spreadsheet yourself, here it is:

Some of the key differences between the plans:

Not every insurance company offers service line coverage yet. It’s getting more popular all the time.

Insurance coverage limits are generally higher than the water district plan.

The water district plan is actually a service agreement, not an insurance policy.

Insurance has deductibles. The water district service agreements don’t.

No waiting period for insurance. 30 day wait for service agreements.

Insurance allows you to choose your own contractor. The water district plan requires you to use theirs.

Pre-paid water district service agreements cover the cost to clear blocked pipes. Insurance does not cover maintenance issues like this.

Insurance covers costs to live elsewhere during repairs after a plumbing or sewer disaster. The water district plans do not.

Insurance costs 66% to 90% less than water district plans.

Choose a Water District Plan If: – you prefer to pay more for the security of no surprises. – you don’t want to pick your own contractor.

Choose Insurance If: – you can handle a $500 or $1,000 deductible for a much lower cost. – you want to use insurance for “the big stuff” like crushed lines, not smaller plumbing issues.

If you have questions about Greater Portland Maine property insurance, contact a Noyes Hall & Allen Insurance agent in South Portland. We offer a choice of many of Maine’s best insurance companies. We can help find the best fit and value for you. We’re independent and committed to you.

Most insurance companies in Maine surcharge insurance rates

after you’ve had an at-fault accident. That’s because people who’ve had one accident

are statistically more likely to have another. So should you pay for auto damage

after a small crash yourself, instead of making an insurance claim? Here are

some things to consider before you decide.

Is My Auto Accident

Considered “At-fault”?

In Maine, unless another party is 100% at fault you may share

some fault in the crash. Some examples of 100% at fault could be:

running a red light or stop sign;

hitting you while your car was legally parked

changing into your lane and sideswiping you.

“At fault” doesn’t have to mean 100% at fault. Even if the

other party is mostly at fault for the crash, you are still partially responsible.

If your insurance company pays to fix your vehicle, and isn’t reimbursed by another

insurer, they may charge you for an “at fault accident”.

Is My Accident Damage

Below the Insurance Company’s Threshold?

Some insurers don’t charge for minor at-fault accidents with

no injuries. Common thresholds are $1,000 and $1,500 of total damage to all

vehicles. If your damage is below that amount, they’ll simply pay your claim

and not surcharge your future rates.

Do I Have Accident

Forgiveness?

Several insurers allow you to avoid a surcharge for your

first accident. Most charge extra for that option. Every

insurer uses different rules and calls this coverage something different. It’s

commonly known as “accident forgiveness”. Some insurers only forgive the

accident if you have no violations in the last several years. Interested in

accident forgiveness? Ask your agent to compare their offerings. There are no

standard terms.

How Much Will My

Insurance Increase After an Accident?

If

your accident is:

“at fault”

above the company’s threshold

and not subject to accident forgiveness

your rates will increase at your next auto

policy renewal.

How

much? That depends on:

How much you’re already paying. Surcharges are

usually a percentage of premium. So, they more you’re paying, the higher your

surcharge would be.

How many other accidents you’ve had. Most

insurers charge a higher percentage for each accident within the 5 year

experience period. If this is your second, it will cost more than the first did.

How long the insurance company surcharges for

accidents. Many surcharge for 3 or 5 years. Some charge more the first year and

decrease the surcharge each year until it’s gone.

Based upon what we see, following an accident, your insurance

rates can increase anywhere from 7% to 20%.

Decreased

Transparency in Insurance Rates

Insurance companies used to provide rate manuals to their

agents. The manuals showed accident surcharge factors and told us how they were

applied. Most insurers no longer provide this information. To agents, or even

to their underwriters. Rating has also become much more complex.

Insurance companies now calculate custom rates for each

person, instead of grouping similar people. Your agent can no longer predict

the exact effect an accident will have on your future insurance costs. Even the

insurance company underwriters are in the dark. They can’t answer questions any

better than agents can. It’s far from ideal.

We’re Here to Help

At Noyes Hall & Allen, we recommend that our clients buy

accident forgiveness if they want maximum stability. This helps keep insurance

costs predictable. Most good drivers appreciate that. For answers to your Maine

auto insurance questions, contact a Noyes Hall & Allen Insurance agent in

South Portland at 207-799-5541. We offer a choice of several insurance

companies, so we can help you find the best fit. We’re independent and

committed to you.