Taking care of your car can be expensive. From routine maintenance to the investment in new tires, you may spend a significant amount of money every year on your vehicle. It is logical to wonder if insurance can help with those costs. There are limited situations where your policy can cover new tires.

At Noyes Hall & Allen Insurance, we can help you determine what coverage is a part of your plan. If you need auto insurance in Portland, ME, give us a call to inquire about your options.

When Does Auto Insurance Cover Tires

It is not common for your auto insurance policy to cover the cost of replacing your tires for normal wear and tear. Rather, auto insurance is there to help you in unexpected and accidental situations to minimize the costs. For example, if you are in a car accident, and the tires suffer damage to them because of the collision, and that collision is covered, the insurance company will pay for new tires.

Some types of policies, like collision insurance, may offer limited protections if you strike surfaces that cause damage to the tires, such as significant potholes that bend your rim. You may also turn to your policy for help with vandalism and theft of your tires, assuming you purchased comprehensive insurance coverage.

There are situations where you can purchase tire insurance or roadside assistance. Less common and only available as an add-on to your policy, these can help you to get new tires in place when a covered event occurs.

Get Coverage You Can Count On

Set up some time to speak to our team at Noyes Hall & Allen Insurance now. Learn about the types of coverage we can offer to you. When you need quality auto insurance in Portland, ME, we can help.

Conditional renewal occurs when your insurance company makes changes to your policy that you did not request. These changes can range from minor adjustments to significant alterations. It’s essential to understand what these changes mean for you..

When Do Insurers Use Conditional Renewal?

Insurance companies often change underwriting requirements. They often “grandfather” in-force policies from these changes. But sometimes conditions change dramatically. Then the insurance company decides to make wholesale changes, even to in-force policies. Or, the insurance company may take a specific action on your policy.

Common Conditional Renewal Types

These are the most common changes in a conditional renewal:

Deductible changes – This could mean an increased deductible or the introduction of a new type, such as a separate wind or hurricane deductible.

Liability Limits – Your liability insurance protection might be reduced, for example, from $500,000 to $100,000.

Coverage exclusions or reductions – Certain coverages, like towing or roadside assistance, might be removed or reduced.

Large rate increases – Some states require notification of significant price increases, though this is not the case in Maine.

Why Am I Getting a Conditional Renewal?

Your insurer might be implementing an across-the-board change, such as a new minimum deductible or a wind deductible for any property in a certain location.

Or the underwriter could be taking specific action on your policy. This is usually in response to claims or some condition that they’ve identified. In this kind of conditional renewal the notice will list the reasons.

Is the Insurance Company Canceling My Policy?

No, a conditional renewal is NOT a non-renewal. The insurance company is offering to renew your policy, however with different terms than before. On the other hand, if the insurance company mails you a Notice of Nonrenewal, they are terminating your contract.

Do I Have Options?

You’re not required to accept the conditional renewal, but it might still be the best deal for you. Conditional renewal is often a re-calibration to the market. In other words, your insurance company is doing what most new insurers would do.

However, you can check with your Noyes Hall & Allen agent to see what they think. We offer a choice of several insurance companies. That gives us good perspective on the market so that we can provide personal advice for your specific situation. We like to say we’re independent and committed to you.

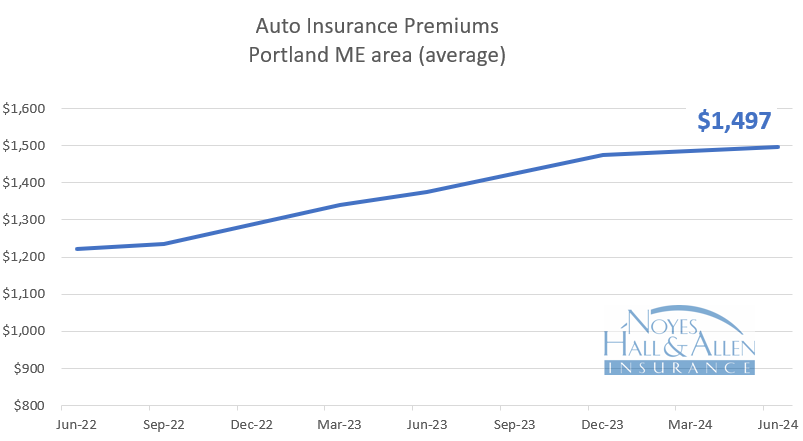

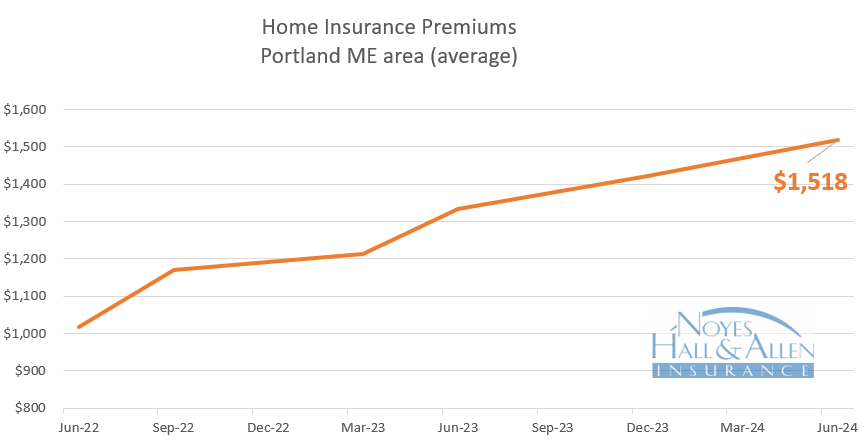

Maine home and auto insurance rates are rising faster than the national average in 2024. Although Maine rates are still among the lowest in the USA, Portland Maine area insurance buyers saw almost a 15% price increase in the first half of 2024. Industry experts expect this to continue through 2024, with some optimism that the increases will be less next year.

Maine Auto Insurance Rates – June 2024

Portland Maine auto insurance rates jumped 13.0% on average in the 2nd quarter of 2024. The average annual auto insurance policy in Cumberland County now costs $1497 per year. Rates vary depending on the type and number of vehicles, drivers and other factors.

Maine home insurance rates continue to increase even faster than auto insurance. The average home insurance premium was 13.7% higher than a year ago. The end is not in sight yet, as US home insurers report record losses from weather events.

Fortunately, historically high rebuilding costs have tempered somewhat. This allowed insurance companies to reduce their “inflation guard” factors. That reduces the percentage increase, which was about 4 percentage points lower than our last survey in December.

Independent Agents Offer a Choice of Maine Home and Auto Insurance Rates

For more than 90 years, Noyes Hall & Allen has helped southern Mainers navigate the insurance market. While we don’t have any control over prices, we offer a choice of several insurance companies. That means we can help you find the best insurance value in any market.

Maine insurance rates follow national and local trends and claim experience. Home and auto rates continue to rise as insurers and customers struggle with rising costs. Portland Maine area insurance buyers saw more than a 15% price increase in 2023. Industry experts expect this to continue in 2024. Still, Maine insurance rates remain among the lowest in the US.

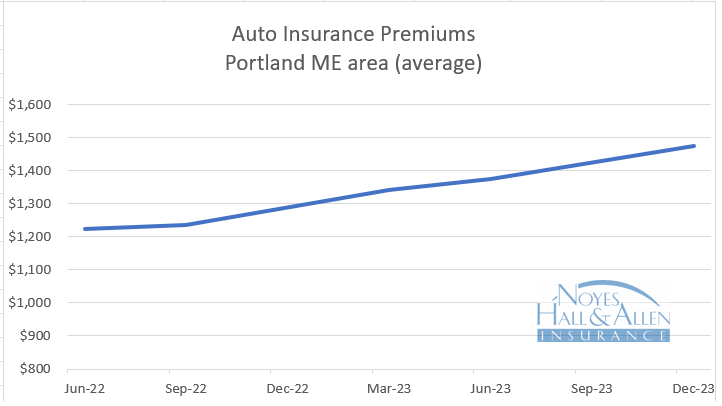

Maine Insurance Rates – December 2023 – Auto

Portland Maine area auto insurance rates jumped 14.4% on average in 2023. The average annual auto insurance policy in Cumberland County now costs $1475 per year.

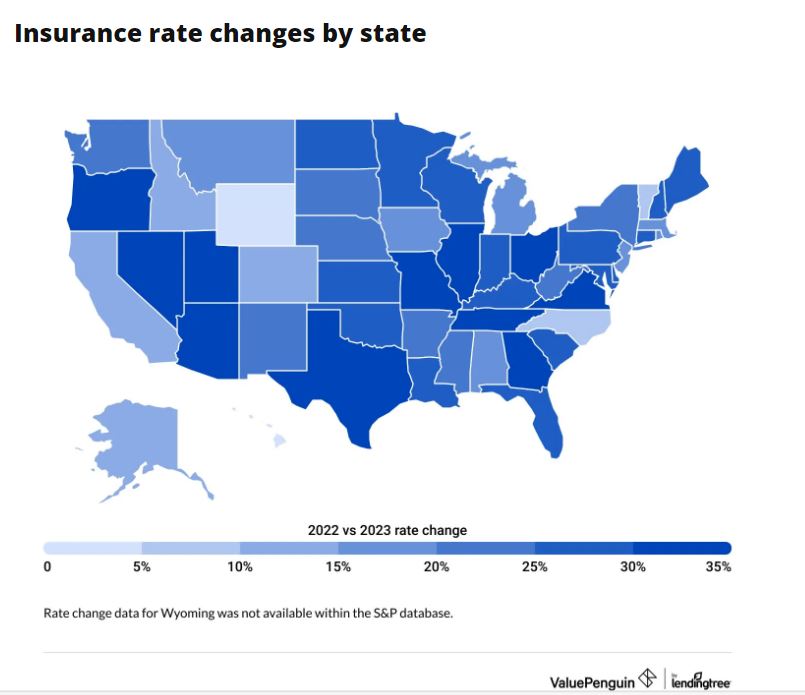

According to a report by Insurify, personal auto prices were up 17% countrywide in the first half of 2023. The Bureau of Labor Statistics reported that auto insurance prices increased 20.3% in 2023. Maine rates increased even more: 28% statewide, according to Insurify. That was the 6th highest rate in the US.

Several factors put strong upward pressure on auto insurance rates everywhere in the US:

Used auto prices are at an all-time high.

New vehicles have much more technology, which makes parts more expensive to replace.

Auto body shops are backlogged, increasing auto rental costs

Auto parts and labor remain scarce, increasing prices

Medical care inflation is high.

Will auto insurance rates level off in 2024? We don’t see any signs that they will. Neither does the financial advice site Motley Fool.

The good news is that Maine auto insurance rates are the lowest in the US according to the Value Penguin “State of Auto Insurance 2024” report. They report that the average Mainer pays $92 per month for car insurance, 44% less than the national average.

Maine Insurance Rates – December 2023 – Homeowners

Maine home insurance rate increases continue to outpace even large auto insurance increases. The average home insurance premium was 17.7% higher than a year ago. The end is not in sight yet, as US home insurers report record losses from weather events and historically high rebuilding costs.

Many of the same insurance inflationary factors described above affect home insurance. But reinsurance costs remain one of the biggest drivers of property insurance rates. Reinsurance is insurance for insurance companies. It protects them against catastrophic losses from natural disasters like wildfires, blizzards, ice storms, hurricanes and tornadoes. Many insurance companies continue to see their reinsurance costs jump 30-50% this year. Insurance companies pass on that cost to their customers.

Although this isn’t great news for Mainers, we’re better off than many areas of the country. Extreme weather has caused wildfires in the west and north, tornadoes and heat in the south and torrential rains elsewhere. Insurance companies have responded by canceling policies in Florida, Louisiana and California, and reducing their new policy offerings elsewhere.

For more than 80 years, we’ve helped southern Mainers navigate the insurance market. While we don’t have any control over prices, we offer a choice of several insurance companies. That means we can help you find the best insurance value in any market.

Maine insurance rates are following national trends. Home and auto rates are up as insurers try to catch up with rising claim costs and construction values. Portland Maine area insurance buyers saw almost a 10% price increase in the 1st quarter of 2023. Even so, Maine insurance rates remain among the lowest in the US.

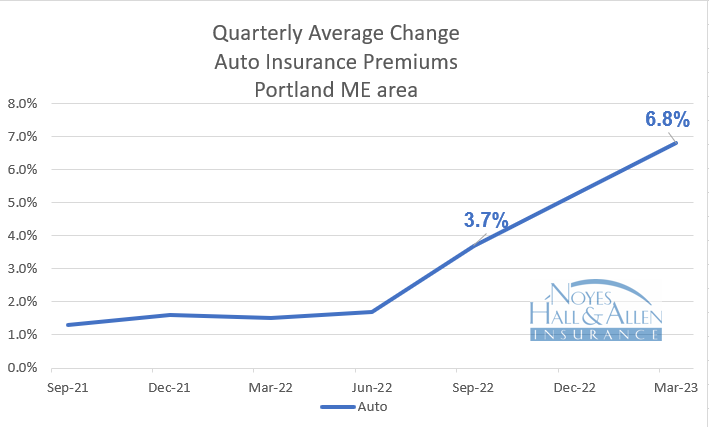

Maine Insurance Rates – Auto – January to March 2023

Between January and March 2023, Portland Maine area auto insurance rates jumped 6.8% on average at renewal, up from 3.7% last September. The average annual auto insurance policy in Cumberland County costs $1341 per year.

Insurers reported higher than expected losses as people drove more after COVID reductions. Body shops and mechanical repair shops charged higher prices due to supply chain and labor shortages. Used auto prices spiked during COVID and settled above pre-pandemic levels. Finally, auto rentals are much more expensive, and needed longer due to body shop delays. All of these factors, along with medical cost increases, put strong upward pressure on auto insurance rates in 1Q 2023.

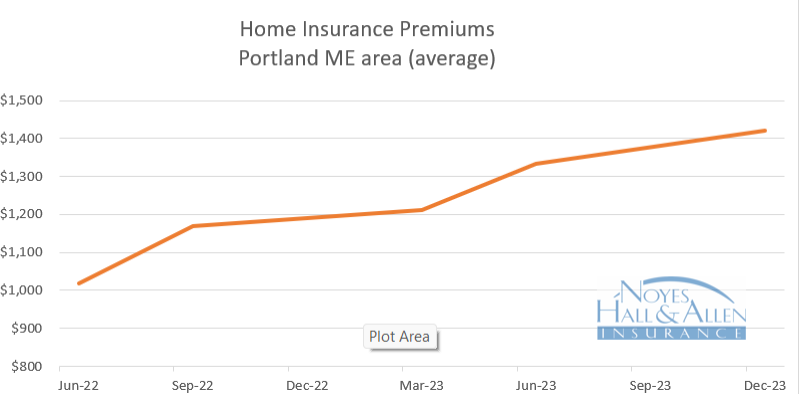

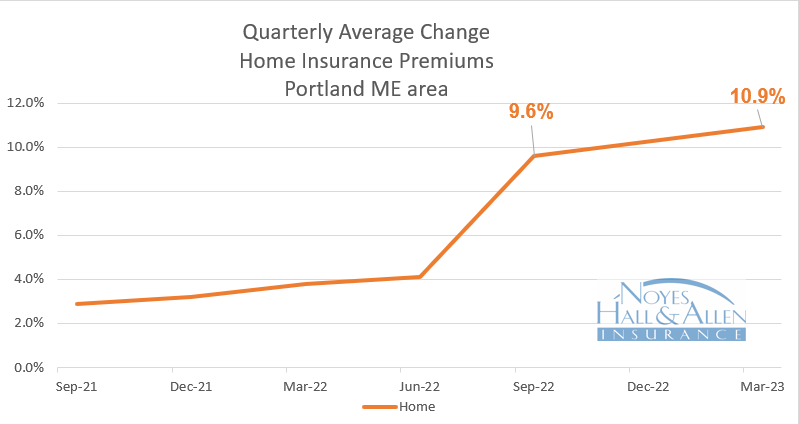

Maine Insurance Rates – Home – January to March 2023

Maine home insurance rates increased even faster than auto insurance. The average home insurance premium was 10.9% higher than a year ago. That’s up from 9.6% in September. And we haven’t seen the end yet.

Many of the same inflationary pressures pushed home prices higher. Building materials and labor costs spiked dramatically during COVID and haven’t settled completely back. It’s been difficult and expensive to find contractors. That delays repairs and increases claim costs.

But reinsurance costs are probably the biggest driver of property insurance rates. Reinsurance is insurance for insurance companies. It protects them against catastrophic losses from natural disasters like wildfires, blizzards, ice storms, hurricanes and tornadoes. Many insurance companies saw their reinsurance rates jump 30-50% this year. Insurance companies must pass on the cost of reinsurance to their customers.

Compare to Find the Best Value

Most financial advisors recommend comparing to get the best insurance value. If you live in southern Maine, you can get up to 5 insurance quotes in 10 minutes from our website. Or contact a Noyes Hall & Allen agent in South Portland at 207-799-5541 for a free no-obligation custom review. We offer a choice of several insurance companies. That means we can help you find the best insurance value.

Should I buy rental car insurance? As a Maine insurance agency, that’s one of our most common auto insurance questions. The answer is a bit complicated. It depends on your risk tolerance, too.

Before we start, 2 important warnings:

This advice applies to Maine insurance policies only. Auto policies vary by state. Check with your insurance company about your own policy.

Auto rental contracts differ. Read yours carefully to find out what you’re responsible for.

OK. Here are some things to consider when deciding whether or not to buy rental car insurance.

What Kind of Vehicle Are You Renting, and Why?

If you’re renting anything but a car, passenger van, SUV or pickup, buy the insurance from the rental car agency. Your Maine personal auto policy will not cover you properly. Likewise, if you’re renting a vehicle for business use, or in a business name, buy insurance from the rental car company.

Where Are You Renting?

U.S. auto policies only cover you in the U.S., its possessions and territories, and Canada. If you’re renting anywhere else, buy rental car insurance from the rental company.

What is Your Risk?

You face four types of risk when you rent a vehicle: liability, collision, injury and lost income for the rental company. Let’s look at the types of coverage that the car rental companies offer.

Rental Car Insurance – Liability

If you are at fault in a crash, you’re liable for any damage or injury you cause. Rental car companies sell Liability Damage Waiver insurance. That means they take responsibility for your action, provided you were operating with in the terms of your rental contract.

Maine auto insurance policies extend your liability protection to rental cars. Therefore, it’s not usually necessary to purchase Liability Damage Waiver from the rental car agency. You usually already have coverage under your own insurance. An exception might be if you have purchased very low liability limits.

Rental Car Insurance – Collision

If you crash a rental car, you’re responsible for the cost to fix it. If it’s stolen while you rent it. You’re responsible to replace it. Car rental companies sell “Collision Damage Waivers” (CDW) to remove that risk. This waiver is not insurance. It’s simply a promise from the rental car agency that they won’t make pay to repair or replace it. CDW is also expensive: often $10 to $30 per day.

Some states also allow the rental car company to claim diminished value. That’s the difference between the car’s value before the crash and after it’s fixed. Maine auto insurance policies are not required to cover diminished value.This is a gap, and a risk that you should think about before declining CDW.

Injury

Rental car company insurance usually doesn’t cover injuries to people in your vehicle. Your Maine auto insurance policy provides medical payments coverage, which is likely a small amount. Regular medical insurance (if any) takes over from there. Otherwise, your medical bills for crash injuries must be paid out of pocket.

Lost Income to Rental Car Company

If you damage a rental car, the rental company has to pull it from the fleet until it’s repaired. That means they lose income. And that’s your responsibility.

Rental car companies sell Loss Damage Waivers (LDW). Similar to the CDW, these are not insurance. They transfer the risk of the lost income from you to the rental company. These cost about as much as Collision Damage Waivers: up to $3,000 per year if you annualize it!

Maine Law requires your auto insurer to cover verifiable loss of use for the rental company up to 30 days. That’s fine as long as the rental company doesn’t claim more than 30 days lost income. With supply chain issues and labor shortages, repairs can often take more than 30 days. You could still be responsible for loss of income beyond 30 days. This is a gap, and one you should consider before declining to purchase LDW.

Rental Car Insurance Tips

Check the Vehicle

Protect yourself by checking the car carefully for damage – with a rental company employee present – before you leave the lot and when you return it. Request that all prior damages be noted in writing. We’ve heard about car renters being charged for damage weeks after turning in vehicles. If you didn’t have an attendant check the vehicle when you returned it, there’s no way to prove your innocence.

Read the Contract

Rental contracts differ. Be sure you understand:

Your responsibilities

Who can drive the vehicle

Any restrictions or requirements (alcohol or drug use, types of roads driven, etc.)

Rental Car Insurance: Budget vs. Risk

Buying the waivers from the car rental company is the safest way to reduce your risk. But it’s expensive. Weigh the cost of those waivers against the additional risk you assume by not buying them.

Maine insurance rates remain among the lowest in the US. But home and auto rates are up as insurers struggle with rising claim costs and rising construction values. Portland Maine area insurance buyers saw increasing prices in the 3rd quarter of 2022.

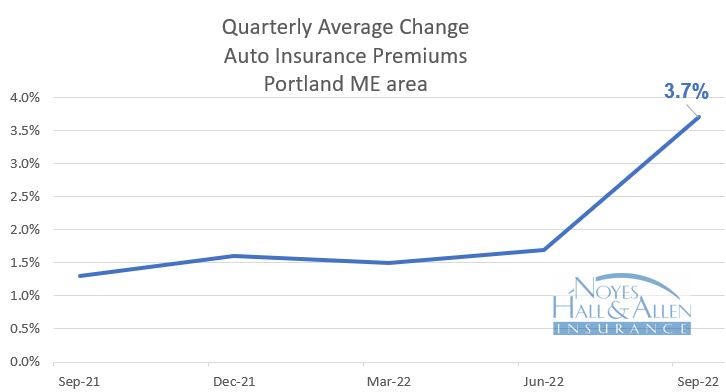

Maine Auto Insurance Rates – June to September

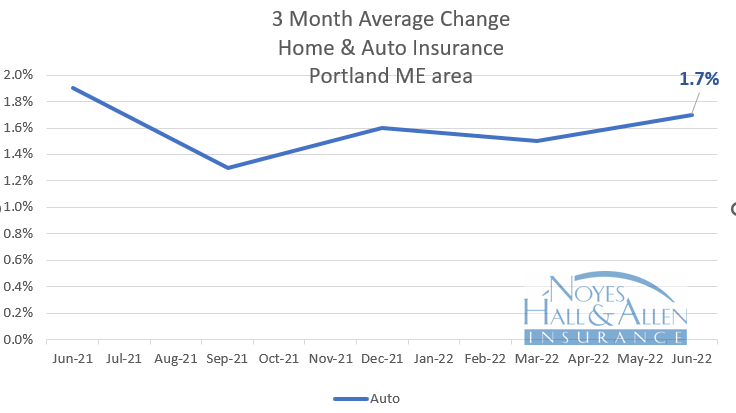

Between June and September 2022, Portland Maine area auto insurance rates averaged a 3.7% increase at renewal, up from 1.7% last quarter. That’s still below the national average of 4.3%.

About 62% of auto insurance buyers experienced an increase in premium. The other 38% saw premiums the same or less than before. Higher repair costs, delays finding replacement parts and increased driving speeds are all factors insurance companies site when they have to increase rates. Customers’ rates might decrease if accidents and violations “age off” or they choose to reduce or remove coverage on vehicles.

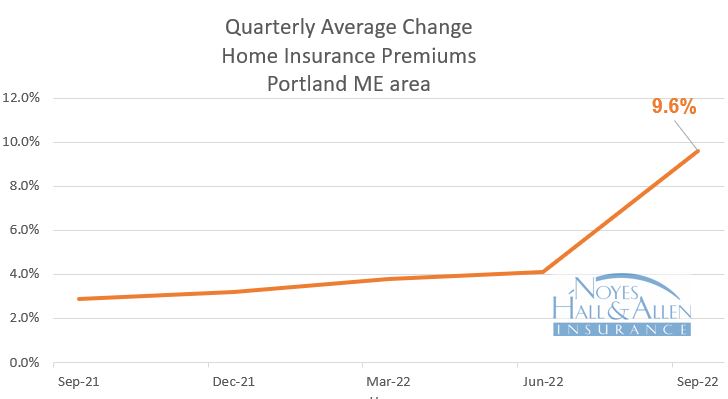

Maine Home Insurance Rates – June to September

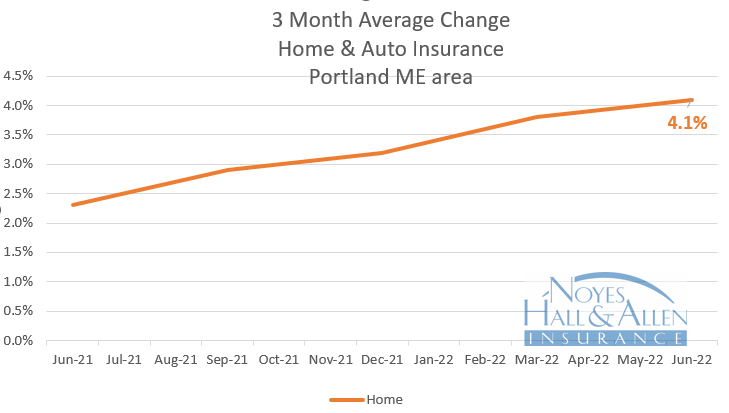

Portland Maine home insurance renewal rates increased 9.6% from June to September. That’s rising faster than auto premiums, and an increase from last quarter’s 4.1% clip. That’s still less than the national average.

Home owners were more likely than auto insurance customers to see a rate increase: 91% saw a renewal increase. Only 9% saw rates stay the same or decrease. Higher building costs contributed to increased rates. So did longer rebuilding times due to labor shortages. The cost to rent temporary housing is very high now. That drives property insurance rates higher. So does the increasing cost of property reinsurance. That’s affected by disasters and other uncertainties.

Maine insurance rates are some of the lowest in the US. But home and auto rates are up as insurers struggle with rising claim costs and rising construction values. Fortunately, Maine insurance buyers are seeing smaller rate increases than much of the country.

Maine Auto Insurance Rates

As of June 2022, Maine auto insurance rates are averaging a 1.7% increase at renewal. That’s considerably less than the national average of 4.3%. The Wall Street Journal recently reported increases as high as 20%.

The main factors driving auto insurance increases include:

More driving. Miles driven are returning to near pre-pandemic levels

More serious crashes. Traffic fatalities reached a 16-year high last year.

Higher repair costs. Parts and labor costs have both risen sharply due to staffing issues, shipping problems and supply chain glitches.

Higher used car prices. When insurance companies total a vehicle, they have to pay the current used car market price. Used car prices went through the roof recently.

Car rental issues. Auto body repair times are much longer. That means longer replacement rentals. Daily car rental costs have spiked, too.

Maine Home Insurance Rates

Maine home insurance rates are rising faster than auto premiums, at a 4.1% clip. That’s still less than the 6% national average. And at an average premium of $1005 per year, Maine home insurance is a relative bargain.

Home insurance costs are affected by building values and claim costs.

Rebuilding costs. Building materials and labor costs spiked during the pandemic. Insurance companies have increased their “inflation guard” factors to provide increased coverage on renewals.

Longer repair times. Contractors are hard to find, too, which increases additional living expenses.

Unusual weather.Natural disasters caused $116 Billion in insured claims in 2021. Maine sees far less than the rest of the US. That’s one reason why our rates are lower. But insurers are feeling less certain about predicting future losses.

Individual Home and Auto Insurance Rates Vary

Every insurance company files their rating plan with the Maine Bureau of Insurance. That plan includes individual rating factors such as driving record, insurance claim history, property location and personal insurance scores.

Does car insurance include roadside assistance in Maine? It’s a common question.

Off the shelf auto insurance policies do not include roadside assistance. But many insurance companies offer it as an option. Others offer towing coverage. Both are less expensive that auto club options.

Are Roadside Assistance and Towing Insurance the Same?

Insurance companies have offered towing coverage for years. Roadside assistance is newer. They’re not exactly the same thing.

Roadside assistance and towing cover many of the same things. Examples are: flat tire repair; jump starting; fuel delivery; and towing, of course. The difference is that towing coverage reimbursesyou after the service call. You have to arrange your own service provide. Coverage is limited to a flat dollar amount, often $75.

Roadside assistance is a service. You don’t usually pay at the scene. If you need assistance, you call a special number and provide your policy info. Some insurers have their own app that you can use to summon help. They dispatch a truck to come and help you. Some roadside plans have a dollar limit per disablement. Most use a towing distance limit – often 25 miles.

How Much Does Roadside Assistance Cost on an Auto Insurance Policy?

Each insurance company sets its own rates. In Maine, expect to pay between $10 and $20 per vehicle per year for roadside assistance. Towing coverage usually costs less than $10 per vehicle for a $75 limit.

Do You Need Roadside Assistance or Towing Coverage if You Have AAA or Onstar?

Most people choose not to have both. They either buy roadside assistance on their auto insurance, or another road service.

Some clients choose to buy towing insurance even though they have another service. For example, some subscription plans charge extra to tow more than 25 miles. If that happens, they pay the excess and submit the bill to their insurance under towing coverage.

Answers to Maine Auto Insurance Questions

Live in southern Maine? Have questions about roadside assistance or auto insurance? Call a Noyes Hall & Allen agent in South Portland at 207-799-5541. We offer a choice of many of Maine’s most popular insurance companies. Many of them offer optional roadside assistance coverage. We’ll help you find a solution that fits your needs and budget. We’re independent and committed to you.

Replacing a car with a new one is an easy insurance transaction. Here’s the info your agent needs to do it:

3 Things Your Agent Needs:

VIN – The Vehicle ID Number for the new vehicle. It’s 17 digits long. That’s easy to transpose. And lots of letters and numbers sound alike, so they’re easy to get wrong. A photo of the VIN simplifies the process and reduces mistakes. Text it to your agent, or email it to them.

Finance Info – Did you buy the vehicle outright? Congratulations! Your agent doesn’t need anything. But if you lease it or take out a loan, they do. The name and address of the finance company will be on your title application. Email or text a photo to your agent. Or, you can call with the info.

Aftermarket Safety or Security Options – The VIN contains details about what’s on your vehicle when it comes off the assembly line. If you purchased add-ons at the dealership, let your agent know. That might include subscription items like OnStar. Or an after-market alarm system.

Do you live in Southern Maine and have questions about auto insurance? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We’re independent and committed to you.