Even the most committed Portland Maine “buy local” fans occasionally buy online. The holiday season will soon be in full swing. That means more shopping, and more opportunity to be a crime victim. Porch pirates are a problem even in Maine, especially during gift-giving season. Maine’s long winter nights provide more of the darkness that thieves love.

Don’t let your joy from the “truck of happiness” turn into the frustration of a box stolen from your porch. Here are some ways to protect your valuable purchases.

Sign up for Tracking Alerts

Most online retailers offer shipment notifications via text, email or smart speaker. Many notify you the very minute your package arrives. Expecting a valuable shipment? Arrange for a trusted friend or neighbor to retrieve and hold it in a safe place until you get home.

Choose an Occupied Delivery Address

Thieves are more likely to target empty or dark homes. Have orders shipped to your work, or the home of a friend or relative who’ll be there to get it. Some online sellers have secure locker facilities or pickup locations. Others allow for pickup at the post office or other shipping store.

Install Smart Home Security

There are so many smart home camera, microphone and monitoring solutions now. Doorbell cameras; motion sensing lights and monitors; whole house security systems. The choices seem limitless. Many allow you to control and watch from a mobile phone or computer. Any option you choose is better than no security at all to reduce your theft risk.

If You are a Porch Pirate Victim

- Notify the police. They may be aware of theft rings in your area. Even if they can’t recover your stolen goods, they can alert your neighbors and save them from the trouble.

- Notify the seller or credit card company. Some online retailers or credit card plans may provide a refund or replace your stolen item.

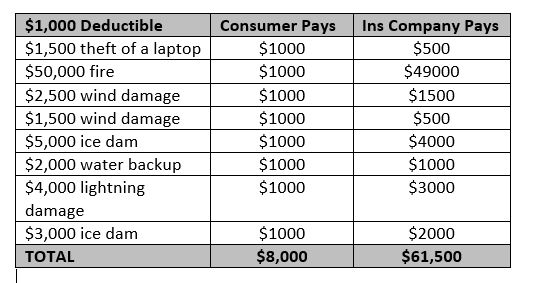

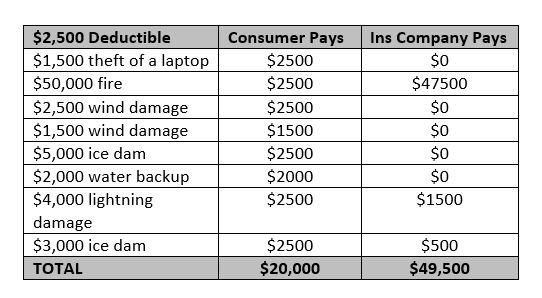

- Call your insurance agent. Home, condo and renters insurance usually cover theft. If your loss was greater than your deductible (often $1000), notify your agent.

Answers to Your Maine Home Condo and Renters Insurance Questions

Whether you live in a Munjoy Hill condo, West End apartment or suburban house in Falmouth or Scarborough, we have answers to your Maine property insurance questions. If you live in Greater Portland, contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541.

Not ready to talk to an agent yet? Get 5 free Maine home insurance quotes online at our website. We’re independent and committed to you.

Having the right home, condo or renters insurance policy is an essential step toward protecting your most valuable asset. It’s an important tool that will protect you and your family financially should a disaster occur. Home insurance policies allow you to recover following events such as fires, weather damage, theft or vandalism. They can also help with the replacement of structures on your property if they are destroyed. The coverage you need depends on your situation. That is why it is important to get to know your agent at Noyes Hall & Allen Insurance. They serve the Portland, ME area, so they understand the challenges that Maine homeowners face.

Having the right home, condo or renters insurance policy is an essential step toward protecting your most valuable asset. It’s an important tool that will protect you and your family financially should a disaster occur. Home insurance policies allow you to recover following events such as fires, weather damage, theft or vandalism. They can also help with the replacement of structures on your property if they are destroyed. The coverage you need depends on your situation. That is why it is important to get to know your agent at Noyes Hall & Allen Insurance. They serve the Portland, ME area, so they understand the challenges that Maine homeowners face. Maine Retirees Are:

Maine Retirees Are:

My Insurance Shopping Nightmare

My Insurance Shopping Nightmare

Insurance Companies Now Sell Underground Line Coverage

Insurance Companies Now Sell Underground Line Coverage