Maine insurance rates are affected by national and local trends. Home and auto rates continue to jump as insurers and customers struggle with rising claim costs and construction values. Portland Maine area insurance buyers saw almost a 15% price increase in the 2nd quarter of 2023. Still, Maine insurance rates remain among the lowest in the US.

Maine Insurance Rates – April to June 2023 – Auto

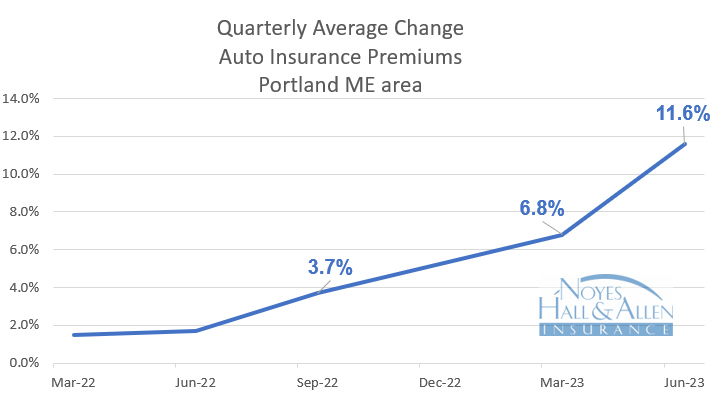

In the 2nd quarter of 2023, Portland Maine area auto insurance rates jumped 11.6% on average at renewal, up from 2% a year ago. The average annual auto insurance policy in Cumberland County costs $1374 per year.

According to a report by Insurify, personal auto prices were up 17% countrywide in the first half of 2023. Insurify says that Maine rates increased even more: 28% statewide. That was the 6th highest rate in the US.

Insurers continued to report higher than expected losses as body shops and mechanical repair shops passed along higher costs. Used auto prices spiked during COVID and settled above pre-pandemic levels. Finally, auto rental times remain very long as body shops require much more time to schedule repairs. All of these factors, along with medical cost increases, put strong upward pressure on auto insurance rates in 2Q 2023.

Maine Insurance Rates – Home – April to June 2023

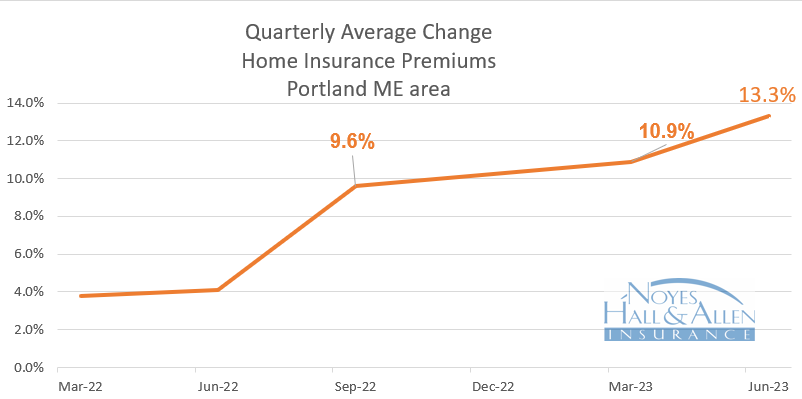

Maine home insurance rate increases continue to outpace even large auto insurance increases. The average home insurance premium was 13.3% higher than a year ago. That’s up from 4% a year ago. The end is not in sight yet.

Many of the same inflationary pressures pushed home prices higher. Building materials and labor costs have dropped from post-COVID peaks, but remain historically high. It’s been difficult and expensive to find contractors. That delays repairs and increases claim costs.

But reinsurance costs remain one of the biggest drivers of property insurance rates. Reinsurance is insurance for insurance companies. It protects them against catastrophic losses from natural disasters like wildfires, blizzards, ice storms, hurricanes and tornadoes. Many insurance companies continue to see their reinsurance costs jump 30-50% this year. Insurance companies must pass on that cost to their customers.

Although this isn’t great news for Mainers, we’re better off than many areas of the country. Extreme weather has caused wildfires in the west and north, tornadoes and heat in the south and torrential rains elsewhere. Insurance companies have responded by canceling policies in Florida, Louisiana and California, and reducing their new policy offerings elsewhere.

Compare Your Options with an Independent Agent

Most financial advisors recommend comparing to get the best insurance value. If you live in southern Maine, you can get up to 5 insurance quotes in 10 minutes from our website. Or contact a Noyes Hall & Allen agent in South Portland at 207-799-5541 for a free no-obligation custom review. We offer a choice of several insurance companies. That means we can help you find the best insurance value.

We’re independent and committed to you.