Many home owners in Maine transfer some of their property to a living or family trust. Trusts can be a useful estate planning tool. Once they were used only by the wealthy. Today, people of all financial means place property in trusts.

Trusts are legal documents. Your attorney can explain if a trust is a good solution for you. They can also help you establish a trust.

Insuring Property in a Trust

How can you insure real estate owned by a trust? It depends on the use of the property. Is it your primary home? A vacation home? Does someone who’s not a trustee live in the home? Is the property owned by a family trust, and used by several relatives?

Each insurer has different requirements for trust-owned property. An experienced insurance agent can help you find the right insurance solution. Independent insurance agents offer a choice of several insurance companies.

Some insurance companies use special policy endorsements for trusts. Others simply add trusts as an “additional insured” on the policy.

Are you living in a trust-owned property in Southern Maine? Are you a trustee? If so, contact Noyes Hall & Allen Insurance in South Portland at 207-799-5541. We offer a choice of Maine’s preferred property insurance companies. We’re independent and committed to you.

by Kayla Bachelder, Concierge Agent, Noyes Hall & Allen Insurance

Ahh, a stormy night at home. Nowhere to be. You’re on the

couch with a nice cup of tea, wrapped in your favorite blanket, about to watch

your favorite movie.

What’s that? Did the lights flick—oh no! Power outage!

Silence. The dog growls in the sudden darkness. The cat

springs from his favorite spot on the back of the couch, causing you to spill

your hot tea everywhere. Complete chaos! How long will the power be out? What

will go wrong before the lights come back on?

The Ultimate Defense: Generators

If you have an automatic generator, nothing changes. Critical heating and cooling systems and lights stay on. You continue to sip your tea, pet your cat and watch your favorite movie (some insurers offer a homeowners discount for automatic generators – ask your agent).

If you have a portable generator, it takes a few

minutes to hook it up. Then you can power your most important appliances and

lights. You may now carry on with your night.

Tips for portable generator owners:

Save instructions for properly setting up your generator. Don’t rely on your memory to do it safely.

Power outages can be unpredictable, and you never know how

long your power may be out. Always be prepared.

Prune trees back from your house. Even healthy tree limbs can succumb to wind or ice storms. Reduce the risk of damage or loss of electricity. Remove limbs that overhang your home, fences or driveway.

Keep your chimney clean. People who rarely use their fireplaces or wood stoves often postpone chimney cleaning. During ice storms, we’ve seen house fires caused by dirty chimneys.

Always have plenty of fuel for your generator and any outdoor cooking appliances.

If you have an electric sump pump, consider installing a gravity activated backup.

Create an emergency blackout kit. Store it somewhere accessible. It won’t be helpful in the back of a closet, or out in the shed.

Emergency Blackout Kit Essentials:

Basic first-aid supplies

Flashlights (avoid using candles)

Drinking water

Extra batteries

Emergency numbers & contacts (incase your cell battery dies)

Backup supplies for your children and pets: diapers, food, etc.?

Canned food is always good to keep on hand in case you can’t get to a store.

Preparing for a Regional Emergency

After a big storm or other regional emergency, power may be out for several days. Are you prepared?

When a Big Storm is Forecast

Freeze containers of water to help keep refrigerated food cold.

If your water comes from a well, fill your bathtub with water. This will allow you to flush toilets, etc.

If you rely on an electric sump pump to keep your basement dry, lift items off the floor.

When the Power Goes Out

Leave the refrigerator and freezer closed. A Full freezer will hold food safely for up to 48 hours. A refrigerator will keep food cold up to 4 hours. After that, in cold weather, store food outdoors, in coolers.

Turn off electric appliances that were on at the time. This can help avoid a power surge when the electricity comes back on.

In winter, open kitchen cabinets to allow the warmer air in the house to reach your water pipes. Pipes are often against cold outside walls. Those walls are even colder when the house has no heat or hot water running through the pipes.

If you don’t have a fireplace or wood stove, go elsewhere if the temperature drops too low. NEVER use a gas cook stove or oven to heat your home.

Use gas or charcoal grills or camping stoves outside – never indoors.

When driving, treat an inoperable traffic light like a four way stop.

When the Power Comes Back On

Check cooking equipment and other appliances to make sure

they’re off.

Unsure if your food is still good? Toss it! Better to be safe than sorry. Make a list of the items you discard. Some homeowners insurance policies cover spoilage of refrigerated food. Contact your insurance agent to see if your policy does.

Answers to Your Insurance Questions

Do you live in Southern Maine? Have questions about insurance for frozen pipes or food spoilage? Concerned about water backing up into your basement? Call a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We’re independent and committed to you.

We offer a choice of Maine’s preferred home, condo and renters insurance companies. We can help you find the best insurance value and answer your questions.

Even the most committed Portland Maine “buy local” fans occasionally buy online. The holiday season will soon be in full swing. That means more shopping, and more opportunity to be a crime victim. Porch pirates are a problem even in Maine, especially during gift-giving season. Maine’s long winter nights provide more of the darkness that thieves love.

Don’t let your joy from the “truck of happiness” turn into the frustration of a box stolen from your porch. Here are some ways to protect your valuable purchases.

Sign up for Tracking Alerts

Most online retailers offer shipment notifications via text, email or smart speaker. Many notify you the very minute your package arrives. Expecting a valuable shipment? Arrange for a trusted friend or neighbor to retrieve and hold it in a safe place until you get home.

Choose an Occupied Delivery Address

Thieves are more likely to target empty or dark homes. Have orders shipped to your work, or the home of a friend or relative who’ll be there to get it. Some online sellers have secure locker facilities or pickup locations. Others allow for pickup at the post office or other shipping store.

Install Smart Home Security

There are so many smart home camera, microphone and monitoring solutions now. Doorbell cameras; motion sensing lights and monitors; whole house security systems. The choices seem limitless. Many allow you to control and watch from a mobile phone or computer. Any option you choose is better than no security at all to reduce your theft risk.

If You are a Porch Pirate Victim

Notify the police. They may be aware of theft rings in your area. Even if they can’t recover your stolen goods, they can alert your neighbors and save them from the trouble.

Notify the seller or credit card company. Some online retailers or credit card plans may provide a refund or replace your stolen item.

Call your insurance agent. Home, condo and renters insurance usually cover theft. If your loss was greater than your deductible (often $1000), notify your agent.

Answers to Your Maine Home Condo and Renters Insurance Questions

Whether you live in a Munjoy Hill condo, West End apartment or suburban house in Falmouth or Scarborough, we have answers to your Maine property insurance questions. If you live in Greater Portland, contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541.

Not ready to talk to an agent yet? Get 5 free Maine home insurance quotes online at our website. We’re independent and committed to you.

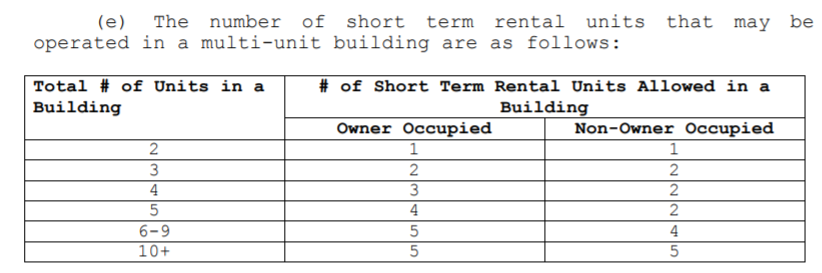

Many cities and towns struggle to balance short term rental with affordable housing. Advocates for short term rental say it encourages property improvements and neighborhood revitalization. They believe private property owners use should be free from government intervention.

Short term rental opponents say owner occupancy and long term leases foster community. They argue that short term rental erodes that community. They also contend that STR contributes to high housing prices. By removing inventory from the market, STR reduces long term housing supply.

Portland, South Portland and Cape Elizabeth Maine are not immune to short term rental controversy. Both passed STR ordinances in 2018 after contentious debate. These laws restrict the time, place and type of short term rental activity. You can find recaps of Portland, South Portland and Cape Elizabeth STR regulations at the bottom of the page.

Insurance for Short Term Rentals in Maine

Thinking of renting your Maine property on AirBnb, HomeAway, VRBO or another short term rental platform? Check with your insurance agent. You may need special insurance to protect yourself. STR platforms also include insurance for hosts. Most of this insurance is supplemental. It’s not intended to replace your primary insurance policy.

If you need insurance for your short term rental property in the Portland Maine area, contact Noyes Hall & Allen Insurance in South Portland at 207-799-5541. If you meet Portland or South Portland’s STR laws, we may help you choose the best insurance value. We’re independent and committed to you.

Portland Maine Short Term Rental Law

This information is current as of 12/1/18 (Code of Ordinances Sec 6-150 et seq.)

Short-term rental operators must register yearly and pay a fee.

Maximum of 400 unhosted units allowed on mainland.

Property owners may register up to 5 STR units combined.

Up to 5 units within primary residence (bedrooms, separate spaces, etc.)

Non-owner-occupied single-family homes and condominium units may not be rented out short term.

Only homes or apartments used as a primary residence can be registered as owner-occupied.

No more than two short-term rental guests are allowed per bedroom. Two more may use other areas for sleeping.

multi-unit buildings have their own rules (below)

South Portland Maine Short Term Rental Law

Current as of 1/1/2019 (Ordinance #22-17/18)

Unhosted non-owner-occupied short-term rentals prohibited in residential zones (single-family home owners may rent their primary homes up to 14 days per year).

Owner-occupied short-term rentals allowed under certain conditions in residential zones.

Requires city-issued registration number in STR advertisement

Short-term rental operators must register yearly and pay a fee.

Short-term rental operators must also be inspected, insured, and licensed by the city and collect Maine sales tax.

No more than two short-term rental guests are allowed per bedroom and six total per occupancy.

Cape Elizabeth Maine Short Term Rental Law

Current as of 1/1/2019 (Zoning Ordinance, Chapter 19)

Apply to Town Code Enforcement Officer for a STR permit.

No permit required for < 14 days per year

For non-owner occupied properties,

No more than 12 tenants at a time from May 1 to October 31

No more than 2 tenants per bedroom.

No more than 8 tenants at a time.

No more than 2 weeks rental per month

7 day minimum rental period

Maine Sales Tax on Short Term Rentals

The State of Maine requires owners of “casual rental” property to pay 9% sales tax. Properties rented fewer than 15 days per year are exempt. For more information about sales tax on short term rental, see Maine Revenue Services Bulletin 32.

When the blows hard many homeowners and business owners discover that their insurance policy has a wind deductible. Windstorm insurance deductibles have been common in the Southern US for years. In Maine, they’re more commonly found on insurance policies for coastal or island properties.

Not every insurance policy in Maine has a separate wind deductible. If your policy doesn’t list one, then your regular property deductible applies to wind damage.

Wind Deductible Amounts – Flat or Percentage

Most homeowners and business property policies have a flat deductible that applies to all causes of loss. These are fixed dollar deductibles. For example if your deductible is $1,000 it applies whether you have a break-in, fire, water or wind damage, you pay the first $1,000.

Many wind deductibles are “percentage deductibles“. The deductible is a percentage of the insurance amount, NOT the actual loss. For example, if your home is insured for $500,000 and has a 1% wind deductible, a $5,000 deductible applies to wind damage, and your flat deductible applies to other causes of loss.

Common Types of Windstorm Damage in Maine

Wind blows a tree onto property, damaging it.

Wind damages roof shingles or siding.

Wind-driven rain lifts shingles and siding, allowing water into the building.

Three Types of Wind Deductible in Maine Insurance

Hurricane deductibles

“Named Storm” deductibles

Wind deductibles

Hurricane Insurance Deductible

A hurricane deductible only applies if your wind damage was caused by an actual hurricane. If your property is damaged by wind during any other kind of storm, the deductible doesn’t apply. Insurance policies define when a hurricane deductible applies. Usually it’s during the time and place that a hurricane watch or warning is in effect.

“Named Storm” Insurance Deductible

“Named storms” include tropical storms and depressions, as well as hurricanes. These occur more frequently, so “named storm” insurance deductibles are more likely to be applied. A homeowner would rather have a hurricane deductible.

Historically, “named storms” were limited to tropical cyclones. But in recent years, the National Weather Service has begun naming winter storms. Does wind damage that occurs in one of these named winter storms cause the “named storm deductible” to apply? That’s unclear. In our South Portland Maine insurance agency, we haven’t heard of an insurance company invoking that. But, it could happen.

Wind Damage Insurance Deductible

Wind deductibles apply to all kinds of wind damage, including those caused by hurricanes, named storms, or other wind. Even moderate winds can cause damage to property. A homeowner or business owner would prefer a hurricane deductible or a named storm deductible to a wind deductible. That’s because windy days happen much more frequently than hurricanes.

Which Insurance Companies Use Wind Deductibles?

Some insurers use only hurricane deductibles. Others use Named Storm deductibles. Still more use wind deductibles. And some don’t use wind deductibles at all.

Each insurance company has its own guidelines. Some large national insurers use a wind deductible for any property within 1 or 2 miles of the coast. That’s a lot of homes in Maine. Many use special deductibles for properties within 1000′ of the coast.

The geography of Maine’s coast varies greatly. South of Portland, much of the coast is low-lying beaches open to the Atlantic. This allows ocean windstorms to affect properties farther from the shore. North of Portland, the coast is more rocky and rugged. Many elevated peninsulas create leeward inlets and protected harbors.

Some insurance companies that understand Maine underwrite these coastal areas differently. They may require a special deductible for properties more exposed to wind, and not for others.

Does Your Insurance Policy Have a Wind Deductible?

If your policy has a separate windstorm deductible, contact Noyes Hall & Allen Insurance in South Portland at 207-799-5541. We offer a choice of many of Maine’s preferred home and business insurance companies. Depending on the location of your home, we may find an insurer willing to insure your property with a flat deductible. This could save you thousands of dollars in case of windstorm damage.

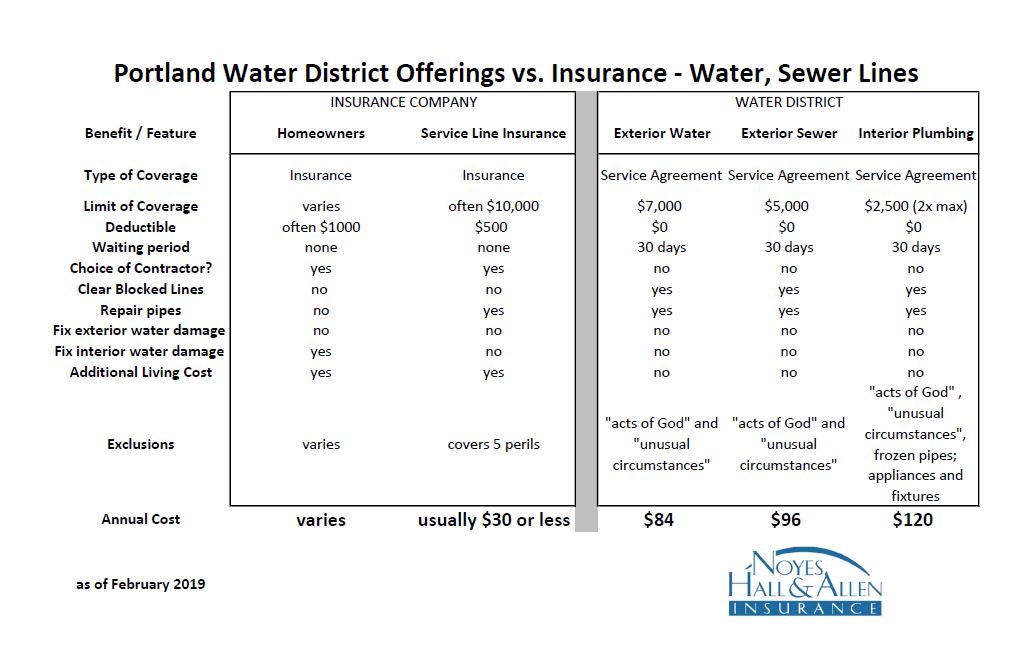

The Portland Maine Water District offers Home Serve service agreement products. There are three options: exterior water lines, exterior sewer lines, and interior plumbing.

Does a water district plan duplicate coverage you already have under your homeowners?

Can you buy water or sewer line coverage from an insurance company?

Is it cheaper to buy water line coverage from an insurance company, or the water district?

We’ve created a spreadsheet comparing what’s covered by the water district plans with what insurance products cover. We’ve also outlined the cost and benefits of each. This 11 minute video reviews it in detail:

If you prefer to look at the spreadsheet yourself, here it is:

Some of the key differences between the plans:

Not every insurance company offers service line coverage yet. It’s getting more popular all the time.

Insurance coverage limits are generally higher than the water district plan.

The water district plan is actually a service agreement, not an insurance policy.

Insurance has deductibles. The water district service agreements don’t.

No waiting period for insurance. 30 day wait for service agreements.

Insurance allows you to choose your own contractor. The water district plan requires you to use theirs.

Pre-paid water district service agreements cover the cost to clear blocked pipes. Insurance does not cover maintenance issues like this.

Insurance covers costs to live elsewhere during repairs after a plumbing or sewer disaster. The water district plans do not.

Insurance costs 66% to 90% less than water district plans.

Choose a Water District Plan If: – you prefer to pay more for the security of no surprises. – you don’t want to pick your own contractor.

Choose Insurance If: – you can handle a $500 or $1,000 deductible for a much lower cost. – you want to use insurance for “the big stuff” like crushed lines, not smaller plumbing issues.

If you have questions about Greater Portland Maine property insurance, contact a Noyes Hall & Allen Insurance agent in South Portland. We offer a choice of many of Maine’s best insurance companies. We can help find the best fit and value for you. We’re independent and committed to you.

More Maine homeowners are installing solar panels. Roof-mounted solar PV panels promise many benefits: decreased electric bills; energy independence; and a reduced carbon footprint.

Are Solar Panels Automatically Covered by Maine Home Insurance?

The good news: your homeowners policy covers your home’s utility fixtures, including heating and electrical systems. Damage caused by fire, wind, falling trees and lightning are all covered.

The bad news: your homeowners policy excludes coverage for some common causes of loss (perils). If squirrels or birds damage your unit, your insurance won’t pay to fix it. And, if your PV solar panels simply stop working, you’re out of luck if you have an “off the shelf” homeowners policy.

Can I Buy Special Insurance for Solar Panels?

Some insurance companies offer breakdown coverage. This covers failure of home systems such as: boilers and heat pumps; appliances; electrical panels – and solar panels. If a system fails prematurely, your insurance company will pay to replace it. But beware: if your system rusts out or simply wears out at the end of its useful life, that’s not covered. And deductibles apply: $500 and $1000 are common.

How Expensive is Solar Panel Insurance in Maine?

Home systems breakdown insurance doesn’t cost much, even though it insures your expensive solar panel installation. It usually costs less than $50 per year, added right onto your homeowners policy.

Do you live in the Portland Maine area? Looking for solar panel insurance or equipment breakdown coverage? Call Noyes Hall & Allen Insurance at 207-799-5541. We offer a choice of Maine’s top insurance companies. Several of them offer this special insurance. We can help you find the best fit for your budget and your home. We’re independent and committed to you.

Insurance companies pool risk. They collect money from many people to pay the losses of a few who have claims. Everyone’s rates go up or down, depending on the insurance company’s experience. More claims paid = higher rates.

You may be wondering:

How much do hurricanes, wildfires and other disasters affect insurance rates?

Do disasters in other states affect my insurance rates in Maine?

It’s helpful to understand how insurance companies price their product. Insurance rates are recommended by insurance company actuaries. They project how much money the insurance company must collect to pay claims and make a profit. This requires complex modeling and formulas. Actuaries recommend rate changes to a special committee of company executives. The committee compares the actuary’s recommendation to the company’s profitability and growth targets. They agree on a proposed rate change, and submit it to Maine insurance regulators.

The regulator’s job is to make sure that insurance rates are:

Adequate to pay claims

Not excessive

Not unfairly discriminatory.

Regulators may approve or deny the rate change, or ask for more information.

What Factors Affect Insurance Rates?

At its simplest, insurance is “money in…money out.”

Money In = Premium Collected

Cheap insurance rates may leave the insurance company with insufficient money to pay claims and make a profit. Rates that are too high may send customers fleeing to other insurers.

Money Out = Losses

The most important determinant of insurance rates. More losses than expected puts pressure for the insurance company to raise rates. Fewer losses puts downward pressure on rates.

But here’s the rest of the story:

Insurance Company Financial Strength – Well-managed insurance companies keep adequate reserves to pay claims on a rainy day. Insurers with strong financials can weather a bad year without huge rate increases. Weaker ones need more frequent rate adjustments. The best way to learn the financial condition of an insurance company? A.M. Best tests the financial strength of insurers and assigns them a letter grade.

Type of Insurance Company – Mutual insurance companies are owned by their customers. After they pay claims, mutuals store their profits to pay future claims. Other insurance companies are stockholder owned. Stockholders expect a return on their investment. Investors pressure executives of publicly held companies to improve profits every quarter. This can lead to larger or more frequent rate increases to stay ahead of current losses.

Reinsurance – Almost every insurance company is also an insurance consumer. They buy insurance against “the big one”. This is called reinsurance. Most companies reinsure against annual total losses exceeding a certain amount. This dampens the impact of multiple hurricanes, fires or other disasters in one year.

Generally, larger insurers buy less reinsurance than smaller ones. Smaller insurers have less surplus, and thus are more vulnerable to catastrophic losses.

Of course, reinsurers are also insurance companies. They must collect more premium if they suffer unexpectedly large claims. Insurance companies pay different reinsurance rates based on their individual loss experience.

Do Disasters in Other States Affect My Insurance Rates?

Probably not as much as you think. Maine insurance regulators only allow insurers to file rates based upon Maine premium and losses. Claims that a company pays in California or Florida are not baked into Maine insurance rates.

BUT…

Insurance companies factor nationwide overhead costs into Maine rates. Cost like advertising, salaries – and reinsurance. Since events outside Maine influence reinsurance costs, they influence Maine customers’ rates. Just less than you might expect.

Having the right home, condo or renters insurance policy is an essential step toward protecting your most valuable asset. It’s an important tool that will protect you and your family financially should a disaster occur. Home insurance policies allow you to recover following events such as fires, weather damage, theft or vandalism. They can also help with the replacement of structures on your property if they are destroyed. The coverage you need depends on your situation. That is why it is important to get to know your agent at Noyes Hall & Allen Insurance. They serve the Portland, ME area, so they understand the challenges that Maine homeowners face.

Liability Insurance Protects Your Assets

One aspect of home insurance to address with your agent is the amount and type of liability insurance that your policy provides. If someone is injured and you are found to be at fault or negligent, you could be held responsible for their medical expense and legal fees if they decide to sue. Injury can be caused by a dog bite, slip and fall, swimming pool accident or even a rock thrown from a lawn mower. This can financially ruin many homeowners. Having the appropriate amount of insurance can prevent this unfortunate situation and help you recover financially. You want to take care of your obligations. An adequate home insurance policy can help you achieve these goals.

Questions About Insurance and Your Personal Liability?

Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. Our knowledgeable staff has worked for a long time with clients throughout Portland and the southern Maine area, so we understand the needs that you, as a homeowner, have. Just checking prices for now? You can get up to 5 instant Maine home insurance quotes by clicking the “get a quote” button above. We offer a choice of Maine’s preferred insurance companies, so we can compare options for you. We’re independent and committed to you. Contact us and get the protection and coverage you need today!

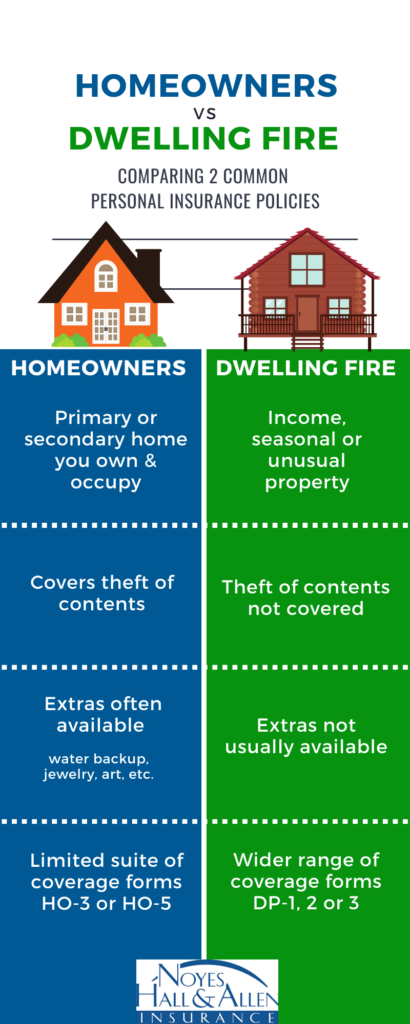

Two types of hazard insurance commonly cover Maine homes and property: a homeowners policy or a dwelling fire policy. Each can satisfy your mortgage company’s hazard insurance requirements. Homeowners and dwelling fire policies provide different coverage. Here are some of the major differences.

Maine homeowners insurance policies are designed for owner-occupied properties, usually one- or two-family homes. Insurance companies look to write homeowners policies on well-maintained year-round homes with good claim history.

Homeowners policies provide coverage for more classes of property than dwelling fire policies. Dwelling fire policies usually provide little or no contents coverage, while homeowners policies aim to cover most of your belongings. You can tailor a homeowners policy for special types of property like jewelry, art or firearms. Specialty belongings like this aren’t well covered by either type of policy off-the-shelf.

Dwelling Fire Policy – A La Carte Coverage Options

Dwelling Fire policies are designed to cover only the things you or the insurance company want to. Is your roof is in poor shape? Your insurance company might exclude damage for water leaks. Own a Maine camp with no plumbing? You don’t need insurance for damage from frozen pipes. Dwelling fire policies allow you to customize your policy by choosing from the basic DP-1 form, the broader DP-2 form, or the broadest DP-3 form.

Other important differences:

Liability coverage is limited to the premises on dwelling fire policies.

Homeowners offer more comprehensive personal liability protection. It follows you worldwide.

Dwelling fire policies also don’t cover theft of contents. These characteristics make dwelling fire insurance policies ideal for tenant-occupied homes or income properties in Maine.

Almost all homeowners policies cover theft of contents.

Comparing Homeowners and Dwelling Fire Policies

Hazard Insurance in the Portland Maine Area

Do you live in Portland or the southern Maine area? Do you own rental or income property? We’re happy to answer your questions about hazard insurance for your mortgage lender, homeowners insurance or dwelling fire insurance. We can explain the difference between various policies. We offer a choice of several insurance companies, so we can shop and compare insurance for you, and help you choose the proper insurance to meet your needs. We’re independent and committed to you. Call Noyes Hall & Allen at 207-799-5541, or click the “get a quote” link above.

Was This Post Helpful?

We provide this information to educate people about insurance options. We hope it was helpful. If so, would you help us in return? If you provide an online review, it would help other people who are looking for help with their insurance. Thank you!

Having the right home, condo or renters insurance policy is an essential step toward protecting your most valuable asset. It’s an important tool that will protect you and your family financially should a disaster occur. Home insurance policies allow you to recover following events such as fires, weather damage, theft or vandalism. They can also help with the replacement of structures on your property if they are destroyed. The coverage you need depends on your situation. That is why it is important to get to know your agent at Noyes Hall & Allen Insurance. They serve the Portland, ME area, so they understand the challenges that Maine homeowners face.

Having the right home, condo or renters insurance policy is an essential step toward protecting your most valuable asset. It’s an important tool that will protect you and your family financially should a disaster occur. Home insurance policies allow you to recover following events such as fires, weather damage, theft or vandalism. They can also help with the replacement of structures on your property if they are destroyed. The coverage you need depends on your situation. That is why it is important to get to know your agent at Noyes Hall & Allen Insurance. They serve the Portland, ME area, so they understand the challenges that Maine homeowners face.