Running a business today involves more than managing employees and customers—it also means safeguarding digital assets. In South Portland, ME, businesses of all sizes face increased cyber threats like ransomware attacks, phishing scams, and data breaches. That’s why having cyber liability insurance isn’t just smart—it’s essential.

The Digital Risks You Can’t Overlook

Cyberattacks can still occur even with firewalls, strong passwords, and employee training. A phishing email or weak endpoint can expose sensitive customer data, freeze your systems, or halt operations entirely. For small businesses in South Portland, ME, the impact of a single cyber incident can be financially and reputationally devastating, and recovery isn’t always straightforward.

Cyber liability insurance aids with the financial aspect of recovery. It can cover costs related to business interruption, data restoration, legal defense, and customer notification. Some policies also provide access to IT experts who can guide your response and help you rebuild faster without confusion.

How We Assist Businesses in South Portland, ME

At Noyes Hall & Allen Insurance, we work closely with businesses across South Portland and the surrounding areas to understand their unique risks and goals. Whether you’re a local retailer, healthcare provider, or professional service firm, we help you find the right level of cyber coverage that fits your needs, not a one-size-fits-all solution.

We take the time to clearly explain your options, answer your questions, and help you feel confident in your coverage. And if you ever need to file a claim or adjust your policy, we’re here, local, experienced, and ready to assist.

Cyber threats are real, and they’re not disappearing. Contact Noyes Hall & Allen Insurance, serving Portland, ME, today to protect what you’ve worked hard to build.

Personal injury liability coverage fills an important coverage gap in many policies. Off-the-shelf personal and business liability policies cover Bodily Injury and Property Damage. But you can be sued for reasons that fall between the cracks.

Invasion of Privacy – interfering with someone’s right to be left alone or to control their personal space or information.

Libel – writing, posting or publishing something false or damaging about someone.

Slander – saying or broadcasting something false or damaging about someone.

False arrest – detaining someone without legal authority or justification.

Malicious prosecution – bringing legal action against someone with the intent to harm them. Suing someone without reasonable grounds.

This coverage is not included in the standard homeowners, renters, condo or business liability policies. You can usually add it for a small additional premium.

What Are Some Examples of Personal Injury Liability Claims?

A person posts on Instagram about a negative experience at a restaurant. The restaurant owner sues for libel.

A landlord enters an apartment to check something while the tenant isn’t home. The tenant finds out and sues for invasion of privacy.

At happy hour, a golf club member tells others that a certain member cheats. That member sues the accuser for slander.

A homeowner sees someone in the neighborhood who looks suspicious to them. They call the police and detain them until the police arrive. The person is actually a fellow resident out for a walk. They sue the caller for false arrest.

A parent posts photos online of their child’s soccer game. Another parent sues the poster for invasion of privacy.

A store owner accuses teen of shoplifting. They keep them in the store until the police arrive. Even though the police confiscate the stolen items, the teen’s parents sue the store for false arrest.

A resident puts a large sign on their lawn, against HOA rules. Another neighbor complains. The neighbor with the sign sues the other for malicious prosecution.

What Does Personal Injury Liability Insurance Pay For?

If someone sues you for these types of injuries, Personal Injury insurance can:

Provide an attorney to defend you – even if the claim is baseless.

Pay legal fees and court costs

Pay settlements or judgments

Who Needs Personal Injury Coverage?

Almost everyone is exposed to personal injury liability. For example, if you or a family member:

Live, work or go to school near other people

Have a high-profile job or volunteer position

Use social media

Own income property

Encounter someone with a history of disputes with others.

Liability Insurance in Maine

Do you live or own a business in Southern Maine? Looking for answers about liability insurance? Contact a Noyes Hall & Allen Insurance agent in South Portland. We offer a choice of Maine’s top insurance companies. We’ll do our best to help you find the right coverage within your budget.

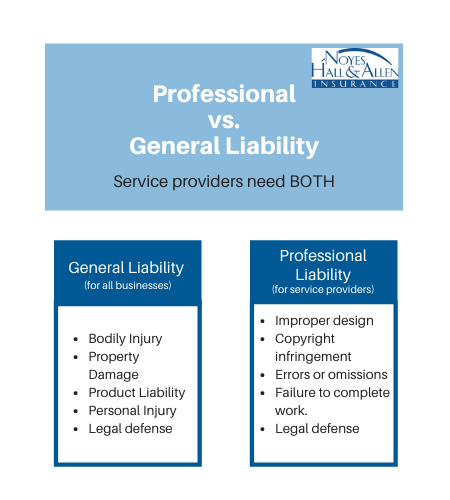

Most Maine businesses have general liability insurance. However, if your business provides a service, you should have professional liability insurance (errors and omissions insurance) as well.

Professional Liability vs. General Liability Insurance

General liabilityinsurance is essential to protect your business assets. It’s also required to get larger jobs. But every business needs GL, from manufacturers to restaurants, contractors to service providers.

General liability protects against damages and legal defense for:

Injury to people

Damage to property

Product liability

Personal Injury, such as invasion of privacy, slander or libel

Professional liabilityinsurance is designed for Maine service providers. It’s sometimes called Errors & Omissions (E&O) insurance, or “malpractice insurance”. Although professional liability insurance is required less often than general liability, it can be even more important.

Anyone who sells their expertise needs professional liability insurance. Whether you’re a tattoo artist, cosmetician, financial service or health care provider, professional liability insurance is for you.

Professional liability insurance protects your assets and your reputation against claims of substandard work. In addition to paying for damages, it also provides defense costs. Some examples of professional liability accusations include:

Work errors or omissions

Failure to complete work

Deadline or budget errors

Improper design

Intellectual property infringement

Who Needs Professional Liability – Maine Examples

Almost every service provider has a professional liability risk.

Examples include:

Medical professionals, including pharmacists

Attorneys and accountants

Real estate and insurance brokers

Drafters, architects and engineers

Consultants of any kind

Hair stylists, tattoo artists, personal trainers and other personal service providers

Because we’re local and independent, we offer a choice of insurance companies. In other words, we can help you find the best value for your insurance protection. Moreover, we can help protect your assets and reputation.

Liquor liability is a risk for Maine businesses and not-for-profits that provide alcohol. Whether your sell or serve, you can be liable under the Maine Liquor Liability Act. You can be responsible for property damage, injury or death caused by the alcohol you provide. Liquor liability insurance can help.

Do I Need Liquor Liability Insurance?

If you don’t SELL alcohol…

Regular business liability coverage may be all you need. Most business general liability policies include “host liquor liability” coverage. That covers you for providing alcohol at a social event where guests aren’t paying for it. For example an open house or special event where drinks are available. Granted, you can still be liable for the effects of alcohol you provide. But you may not need special insurance.

If your business or organization sells or serves alcohol…

You DO need separate liquor liability insurance. Typical examples include

Bars, pubs and taverns

Breweries and distilleries with tasting rooms

Restaurants and cafes

Retail stores

Performance venues

Private clubs

Dance clubs

For instance, someone could claim the alcohol you sold caused injury or damage. While your general liability insurance will not respond, but liquor liability insurance would.

Possible Liquor Claim Examples

Auto accidents – a patron you serve gets behind the wheel and crashes, injuring someone. Or worse. The police test their BAC and find them over the legal limit.

Serving underage patrons, even by mistake.

Altercations or violence – an intoxicated patron (or two) gets into a fight. They injure others as a result. (Note, some liquor liability policies exclude assault and battery).

Serving someone excessively – you can be responsible for their injuries or death.

Serving an obviously intoxicated person – you can be responsible for resulting harm.

Are Damages for Maine Liquor Liability Capped?

The Maine Liquor Liability Act limits damages to $350,000 per incident. But that doesn’t include medical care or wrongful death. Medical care liability is unlimited. Even more, Maine’s Wrongful Death Statute allows up to an additional $750,000

In other words, serving liquor can get you in plenty of trouble. Protect your assets with Liquor Liability Insurance.

How Much Does Maine Liquor Liability Insurance Cost?

Costs vary greatly according to exposure. For example, the smallest liquor liability exposures can cost as little as $250 a year. On the other hand, businesses selling a lot of alcohol can spend several thousand dollars a year.

Cost factors include:

Alcohol sales revenue

Ratio of alcohol sales to other retail sales (stores)

On-premises consumption vs. take-away

Ratio of alcohol receipts to food (restaurants).

How to Reduce Insurance Costs

Meanwhile, controlling those factors are a good way to reduce insurance costs. For example:

Server education training for employees (TIPS, etc.)

Written policies and procedures for servers, with compliance monitored by management.

Strong ID checking procedures

Providing non-alcoholic beverages

“Ride home” alternatives for patrons who appear intoxicated

Keeping a log book of any incidents – or potential incidents

Part of Your Total Insurance Plan

Does your Maine business or organization sell or serve liquor? Talk to a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We can advise whether you need liquor liability insurance. If you do, we can help you incorporate it into your overall insurance program.

Because we’re locally owned and independent, we offer a choice of insurance companies. In other words, we can help you find the best value for your insurance protection. We’re independent and committed to you.

Professional liability insurance and general liability insurance are different. Maine businesses and non-profits may need both. What’s the difference between professional liability insurance and general liability insurance?

What is General Liability Insurance?

GL insurance protects your business’ assets against four types of lawsuits:

firstly, Bodily Injury caused by your actions, or that happen on your premises. For example, slips and falls in a parking lot, or a contractor dropping a hammer from a scaffolding, injuring someone.

secondly, Property Damage that you cause to the property of others. For example, your crew knocks over a valuable vase while cleaning someone’s home.

thirdly, Personal Injury, such as slander, libel or invasion of privacy. For instance, a realtor walks into an occupied apartment without warning.

and finally, Products and Completed Operations Liability – in case your product or work harms someone or their property. An example: a diner gets food poisoning after eating in your restaurant, or your roofing job fails, causing water damage at someone’s house.

Moreover, general liability insurance pays your legal defense costs against these types of suits – even if you did nothing wrong!

What is Professional Liability Insurance?

Professional liability insurance, sometimes called E&O insurance, protects against claims of:

Negligence – for example, a real estate agent fails to disclose a defect in a property, or a planning consultant who misses an important regulation, causing their client to incur large penalties.

Improper or Inadequate work – for instance, copyright infringement, improper design, or a clerical error that costs your client money.

Like general liability, professional liability insurance also pays legal defense costs.

Do I Need E&O Insurance?

Professional liability is a hazard in almost any profession. Some of the most common ones include:

Architects and engineers

Accountants, attorneys and bookkeepers

Beauticians, tattoo parlors and other personal service providers

Condominium and non-profit boards

Consultants and coaches

IT professionals

Marketers, creatives, drafters and designers

Medical and health care professionals

Real estate and property managers

Professional Liability Insurance Questions?

If you have Maine professional liability insurance questions, contact a Noyes Hall & Allen agent for prompt, professional answers. We offer a choice of many of Maines top business insurers. We also have access to dozens of specialty insurers. In other words, we can help you find the best fit and value for your insurance. Because we’re independent and committed to you.

General liability insurance is important for Maine businesses. If you operate a business in Maine, customers or the town may demand a certificate of insurance. This proves that you have general liability coverage. Some people think about liability insurance when they first start their business. However, others don’t think of it until someone asks for proof.

What Does General Liability Insurance Do?

GL insurance protects your business’ assets against lawsuits in four ways:

Firstly, Bodily Injury caused by your actions, or that happen on your premises.

Secondly, Property Damage that you cause to the property of others.

Thirdly, Personal Injury, such as slander, libel or invasion of privacy.

and finally, Products and Completed Operations Liability – in case your product or work harms someone or their property.

How Much Business Liability Insurance Do I Need?

Liability insurance protects your assets. Therefore, you should at least carry enough to protect the net worth of your business. Moreover, you may also need a certain limit of liability coverage to work for a certain client. For example, a $1 million per-occurrence limit is common. Higher limits are available, as are commercial umbrella policies, which provide even higher limits.

What General Liability Insurance Does NOT Protect Against

Professional Liability, such as improper design, malpractice, errors or omissions. You need separate Maine professional liability insurance to get this coverage.

Employment Practices Liability. This covers several HR-related perils. For example, wrongful termination, sexual harassment or employee benefits liability. You should purchase Maine Workers’ Compensation Insurance if you have these exposures.

Auto Liability. You should purchase Maine commercial vehicle insurance if your company owns vehicles. Even if your company owns no vehicles, you should add Hired and Non-Owned Auto Liability coverage to your GL policy.

Pollution Liability. If your business uses pollutants, you should purchase separate insurance for this.

How Much does General Liability Insurance Cost?

Rates vary, starting at a few hundred dollars a year. Yours will depend on many factors, including:

Type of business or operation;

Your revenues or payroll;

How long you have been in operation;

Personal qualifications and licenses;

Prior claims;

Whether you combine your business property insurance with your GL coverage.

Business Liability Insurance Questions?

Do you have Maine business liability insurance questions? Contact a Noyes Hall & Allen agent in South Portland at 207-799-5541 for prompt, professional answers. We offer a choice of many of Maines top business insurers. We also have access to dozens of specialty insurers. In other words, we can help you find the right fit for your organization and budget. Because we’re independent and committed to you.

“Non-admitted” insurance companies are not approved by the Maine Bureau of Insurance. But they play an important role in Maine’s insurance market. Non-admitted carriers are often called “surplus lines” or “excess lines” insurers. They take higher risks than admitted insurers. That comes at a cost. Here are the pros and cons of the non-admitted insurance market.

The Risk of Non-Admitted Insurance

Non-admitted insurance companies’ coverage forms are not approved by Maine regulators. Their customers don’t enjoy many of the Maine Insurance Code’s protections. But they are subject to federal regulation through the Dodd-Frank Act (.pdf, 800+ pages).

In case of insurer insolvency, the Maine Guarantee Fund does not apply. Even if a policy is active, claims might not be paid if the company goes bankrupt.

The Maine Bureau of Insurance doesn’t review or approve non-admitted insurance rates. They do with admitted insurers. Non-admitted insurers may charge what the market will bear.

Many non-admitted insurance policies have a “minimum earned premium” of 25% of the annual premium. Even if you cancel your policy right away, the insurer will keep 3 months’ premium.

Non-admitted insurers may add separate policy fees to premium. Those are usually non-refundable. They must add Maine surplus lines tax to the premium, too.

Non-admitted insurance is often more expensive and provides less coverage. That’s why Maine only allows non-admitted carriers to insure risks that admitted carriers refuse.

Non-Admitted Insurance Can be Valuable

Purchasing insurance from a non-admitted carrier isn’t ideal. But it is a valuable service.

Some protection is better than none. While non-admitted insurance coverage is restrictive, it can protect customers against catastrophe.

Non-admitted coverage can be a temporary solution. It can give you time to make improvements and qualify for insurance from an admitted insurer.

Most lenders will accept non-admitted policies as proof of insurance. Lenders require insurance from their borrowers in order to make a loan.

Be a Smart Insurance Consumer

Purchasing insurance from a non-admitted carrier can be risky. Since non-admitted insurers are not covered by the Maine Guaranty Fund, it’s important to research your insurer’s financial strength. But many non-admitted insurers have excellent A.M. Best financial ratings (.pdf). Ask your agent about yours.

Non-admitted insurance proposals list all applicable exclusions, warrantees and coverage forms. You should at least understand them, even if you can’t change them. Your agent should be able to explain them to you. If you’re a client, your Noyes Hall & Allen Insurance agent can answer questions about your insurance. We’re independent and committed to you.

Buying Portland Maine business insurance doesn’t have to be complicated. If you own a business, it’s important to protect your asset with commercial insurance. These policies can protect your building and vehicles against liability, theft, fire and more.

Whether you just started a business or need to upgrade your existing commercial insurance, the team at Noyes Hall & Allen Insurance has put together this short list to help you get started.

1. Find a Reputable Business Insurance Agent

Working with a friendly and reputable local insurance agent takes the hassle out of buying a new commercial insurance. They will ask you some questions to get a better understanding of what coverage you need.

Many Maine people prefer to do business locally. A good local agent knows the area, and what Maine’s unique hazards and opportunities. They can help you compare quotes, understand your coverage and bundle your policies. Check their online reviews to help you choose.

2. Compare Several Quotes

It’s smart to compare three or more quotes during the commercial insurance buying process to find the right one. Go over each in detail with your reputable agent, asking questions for clarification as needed. Policies will differ on price and coverage so be sure to understand what you’re getting and for what price.

Fortunately, Noyes Hall & Allen Insurance offers a choice of 10 of Maine’s top business insurance companies. That means we can do the shopping and comparison for you, with one stop.

3. Bundle Your Business Insurance Policies

If you need more than one type of insurance, consider bundling with one insurance company. For example, insuring your business vehicles and your property with the same company can simplify billing and save on your premiums.

Own a Portland Maine Area Business?

Have insurance questions? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We offer a choice of many insurance companies and have served the local business community for almost 90 years. We’re independent and committed to you.

Contractors insurance audits are important. They help keep insurance costs predictable for all contractors. They also create important information for insurance rate setters. Accurate payroll and sales figures help them know how much premium they must charge to cover losses.

If your audit results in extra premium, it will be due within 30 days. You want to avoid that if possible. Tell your agent if your payroll, sales or subcontractor costs are much higher than the estimate on your policy.

Why Am I Getting an Insurance Audit?

Many contractors insurance policies in Maine are auditable. Contractors’ jobs, payroll and subcontractor costs vary each year. In slow work years, claims tend to be lower. In boom years, there are more claims. Insurance companies audit to “true up” premiums with the expected claims.

Types of Contractors Insurance Audits

Your insurance company might audit your results in several ways. The method can change year-to-year. It may depend on the size of your business and current conditions.

Online or Mailed Audit – You fill out your own audit on a form and send with quarterly 941 reports.

Phone Audit – An auditor will set an appointment to complete the audit by phone. They’ll tell you the information you’ll need. Commonly, quarterly 941 reports, payroll reports, and a list of officers and owners of your business.

Physical Audit – An auditor comes to your workplace by appointment. They examine your records in person. The auditor also checks that employees are properly classified based on the work they perform.

What Happens if I Don’t Complete My Contractors Insurance Audit?

Workers compensation insurers must report premiums and losses to NCCI. NCCI uses that information to set rates and experience mods. Insurers can incur penalties for slow or inadequate reporting. General liability insurance uses payroll info too. Your audit information is an important factor in insurance company rate-setting.

Insurers are not going to “go away” if you ignore the audit request. Your audit information is time sensitive, and collecting it is someone’s job.

If you fail to respond to audit requests, the insurance company will bill you for an estimated audit. You do not want an estimated audit. It increases your premium by 25% or more. And you’re contractually obligated to pay it.

Bite the bullet. Complete your audit. It’s not going to go away.

How Do I Prepare For an Insurance Audit?

Be ready. Your audit happens at the same time every year.

Keep good records throughout the year.

Get certificates of insurance for your subcontractors: general liability and workers compensation.

Tell your agent during the year about large payroll, sales or subcontractor cost changes, up or down.

Keep track of time and payroll for different kinds of work. This can lower your workers comp costs while still protecting you and your workers. Include overtime.

Remember that some owners or officers might have waived workers comp coverage.

If you have a physical audit, plan to be present and available. The auditor wants to finish their work quickly and thoroughly. The faster they have what they need, the sooner you can get back to work.

Completing Contractors Insurance Audits: Who Can Help?

Completing an online or mailed audit? The insurance company should send detailed instructions. If you’re stuck, you can call the insurance company’s audit department or your agent. Sometimes, your payroll company can assist, too.

What if I Disagree With the Audit Results?

You can dispute an audit if the payroll or classifications are wrong. You can’t dispute just because the premium is higher. Your agent may be able to help, but they don’t have the information unless you authorize the insurance company to share it with them.

Maine Contractors Insurance Answers

Are you a contractor in Southern Maine? Do you have questions about Maine business insurance? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We have decades of experience and offer a choice of Maine’s top contractors’ insurance companies. We’re independent and committed to you.

Portland and South Portland Maine recently passed ordinances expanding outdoor seating options for local restaurants. These respond to indications that coronavirus is less likely to spread outdoors. Soon, some local restaurants will be able to serve patrons :

on sidewalks

in parking lots or closed streets

in on-street parklets.

Transitioning a Restaurant to Outdoor Dining

Outdoor dining isn’t for every restaurant. Depending on your cuisine, location, formality and clientele, you may choose not to serve al fresco. If you do, here are some things to consider.

Check city rules and resources. Portland and South Portland city web sites have the ordinances and applications for permits and street closures.

Up your cleaning game. During the COVID threat, you’re already doing extra cleaning and disinfecting. Outside adds new cleaning challenges: pollen, dust, litter and even insects.

Keep it light – and smooth. Make sure there’s enough light for employees and customers to see well. Paint or tape the edge of irregular surface levels. Avoid loose cords and other trip hazards.

Watch the skies. That includes the sun. Plan your seating to avoid excessive sun exposure during meal service, if possible. Summer thunderstorms can develop fast. Have a plan to quickly evacuate your dining area and secure umbrellas and other furniture. That will help avoid injury and damage.

Beware of vehicles. Create barriers between diners and vehicles – including bikes and scooters that might be on sidewalks.

Watch outdoor flames. Keep propane heaters, cooking equipment and other heat sources away from flammables like fabrics and awnings.

Check your insurance. Many liquor liability policies only cover you “on premises.” Does that extend to a parking lot or street? The same with property insurance for your outdoor seating and fixtures. Ask your agent about your insurance coverage.

Do you own a Portland Maine area restaurant, cafe, food truck, brewery or other food service business? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. We’re local business owners, just like you. We offer a choice of Maine’s top business insurance companies. We’re independent and committed to you.