You created a fabulous signature event for your non-profit. The stakes are high. Your budget – maybe your job – depends on its success. But you’ve done your homework. The board is jazzed. Volunteers, donors and the venue are ready. Publicity and social media are on point. RSVPs and reservations are rolling in.

Now all you need is good luck. Here’s how to stack the odds in your favor.

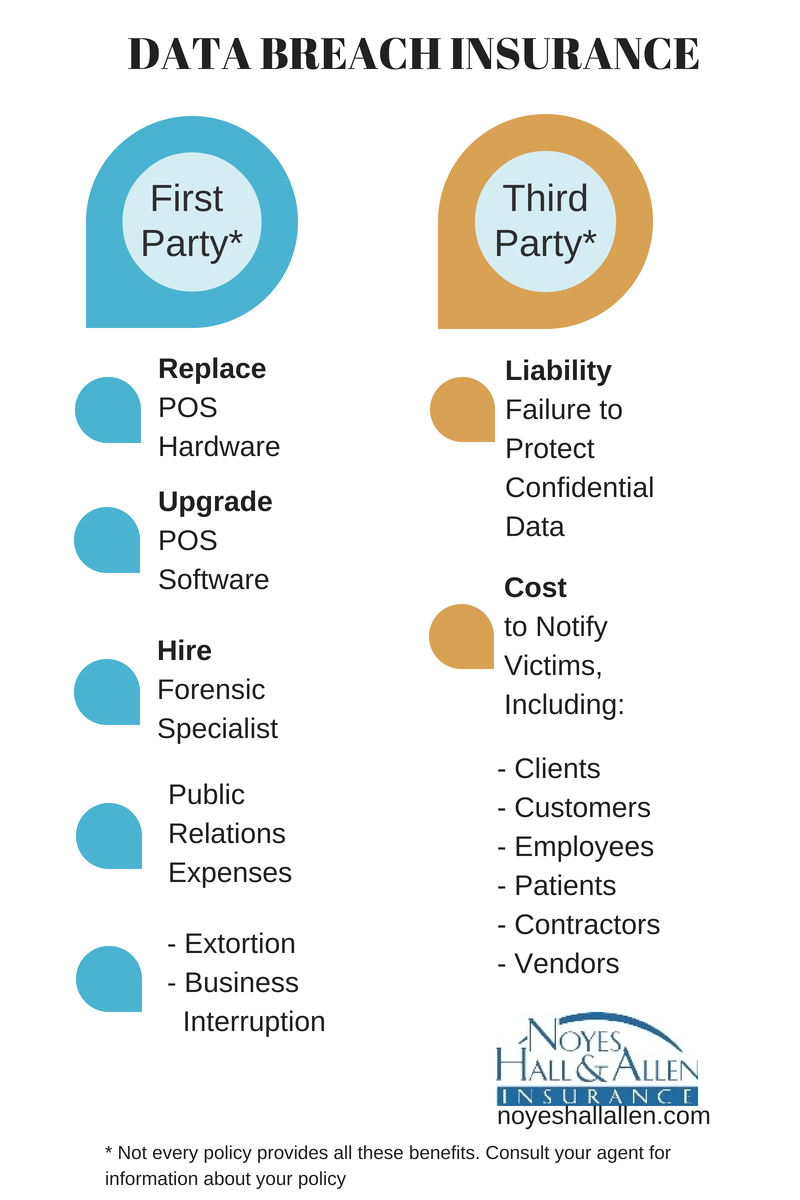

Your Programs Depend on the Event’s Revenue. Protect It

Insure the weather.

Insure the weather.

Does the forecast keep you up at night for weeks before your event? Believe it or not, you can insure the weather. A special insurance policy can reimburse you for lost revenue caused by stormy weather.

How does weather insurance work? Pick the amount of income you want to protect, and a “trigger”. For example, if it snows more than 6” at the event site, your insurance pays the amount on your policy. It might cost a few points of revenue, but it’s better than a big loss if the weather makes everyone stay home.

Hire Out the Risky Stuff

Your non-profit is probably not in the business of tending bar, supervising a road race or shucking oysters. Do yourself a favor: hire a professional. One with their own insurance.

Don’t take on a lot of risk for a little savings. If something goes wrong, those savings are soon forgotten. But the injury or damage you caused to others – and to your reputation – could last a long time.

Protect Donations

Do you collect and store auction prizes and other donations before your big event? Don’t let a broken pipe, fire or theft erase the good they were intended to do. Add them to your insurance policy – and remove them after the event. It doesn’t cost much, and can save a lot.

While we’re at it, make sure you have “money and securities” coverage and “employee dishonesty” coverage. Make sure your organization keeps the funds you worked hard to raise.

Love Your Volunteers

Love Your Volunteers

Your organization would be lost without them. You appreciate the heck out of them. Do you treat them that way? Would you leave them out to dry if they got in trouble from working your event? Does your insurance protect them against lawsuits for injury or damage they cause while volunteering? If not, fix that. Now.

What about board members? Committed directors are hard to find. Does your non-profit have Directors & Officers Liability coverage? Those with considerable assets are more likely to serve if they have protection from lawsuit. Don’t you owe that to them?

Talk to your insurance agent about your event. Explore the coverage we listed above. See what fits your budget. Better to explain to your board that you investigated insurance and chose not to buy it than that you never thought of it.

Noyes Hall & Allen helps Greater Portland non-profits manage their risk within their budget. That allows them to stay true to their mission and avoid financial catastrophe. If you’d like to talk to a Noyes Hall & Allen Insurance agent, call 207-799-5541. We’re independent and committed to you.