Hiring an independent contractor a great way to expand your company’s products and services without adding overhead. The right sub can make you look good.

Subcontractor or Employee?

By Maine law, a worker is an employee unless they meet tests to be an independent contractor. That makes them subject to employment tax and workers compensation. If your Maine business hires independents, here’s what you need to do.

Get Documentation from Subcontractors

Workers compensation charges sub costs as payroll unless you have proof of subcontractor status. That can be a very expensive surprise. And the bill is due in lump sum.

For more Maine Workers Compensation insurance tips, contact Noyes Hall & Allen in South Portland at 207-799-5541. We’re independent and committed to you!

Natural disasters are on the rise, putting business owners at risk of suffering damage or loss of business property. A big disaster can literally put you out of business.

If you own a business in Maine, your customers and employees depend on you to prepare for the worst. Commercial insurance from Noyes Hall & Allen Insurance is one way to protect your business from disaster damage. Here are a few other ways to prep your small business for natural disasters.

Employee Disaster Readiness

Develop a plan for your employees, so they will know what to do in the event of a disaster.

Make sure that employees know who to contact and how to reach key personnel when needed.

Create an evacuation plan that employees can easily follow if they have to escape in a hurry.

Update new employees on disaster readiness so everyone is well-informed on what’s expected of them if disaster strikes.

Communicating with Clients after a Disaster

If your customers can’t reach you after a disaster, they may find someone else who can help. Don’t jeopardize your business. Have a plan to continue your operations, and let your customers know where to find you.

Have a plan in place to communicate with key clients after a disaster.

If your building is severely damaged, you may need to open a temporary location to continue operations. Thinking about possible options before disaster strikes can save valuable time following a disaster.

Protecting Essential Data after a Disaster

Make sure your primary data is backed up digitally to prevent loss in a disaster. This includes financial records, employee and customer information, and any other critical data you need to keep your business running. Cloud backup is the safest, most secure means of protecting essential data from natural disasters.

Commercial Insurance Coverage

Purchase adequate commercial insurance for your building, business equipment, and inventory. Just as important, be sure you have business interruption coverage. Many businesses have enough insurance to replace what they lose, but not enough to recover lost earnings. This can cause your business to fail.

Maine Business Insurance

For information on commercial insurance coverage and costs, contact Noyes Hall & Allen Insurance in South Portland, ME. We offer a choice of Maine’s top business insurance companies. We can help you find the right fit for your business. We’re independent and committed to you.

Commercial insurance protects a company or business owner from losses to buildings or equipment necessary for the operations. However, many Maine businesses rely on portable equipment to operate. So, does commercial coverage offer protection for essential portable equipment when it’s off the premises?

Coverage for Portable Equipment

Commercial insurance covers equipment, inventory and supplies located on the premises of the covered location. However, this may not extend to things that leave the premises. If you bring property to job sites or customer locations, portable equipment insurance may be necessary to prevent gaps and losses.

Portable equipment coverage is sometimes called an Inland Marine Floater. This coverage will protect electronic equipment and other contractor related items required to perform daily work-related tasks. Before selecting additional insurance, speak with an agent about current and future needs, and find out what options are currently available to get a complete layer of protection.

Protect Your Equipment on Job Sites

Considering a purchase of portable equipment for your business? Talk to an agent from an insurance company who can outline what steps are necessary to get comprehensive coverage. Although some protection may be offered by standard commercial insurance, navigating portable insurance coverage may be necessary.

If your business is located in Southern Maine, contact Noyes Hall & Allen Insurance in South Portland at 207-799-5541. We offer straightforward solutions from some of Maine’s top business insurance companies. That allows you to choose insurance that matches your business needs and provide you with peace of mind.

Getting the right combination of insurance to cover a business can be tricky. Don’t risk gaps and issues that could spell disaster. Consult with an agent from Noyes Hall & Allen Insurance to get the coverage necessary to protect a business in Portland, ME and throughout the state.

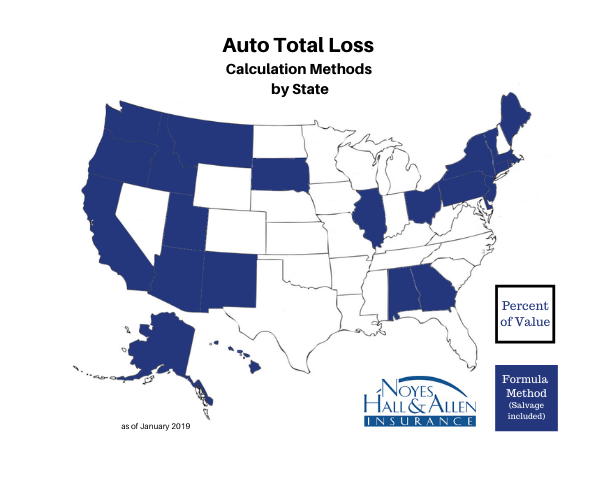

When a crash or disaster seriously damages your vehicle, it’s stressful and confusing. If the damage is bad enough, an insurance company might declare your vehicle a total loss. Fortunately, it doesn’t happen often to most of us. What does it really mean when your vehicle is totaled?

What Does it Mean When a Vehicle is Totaled?

A vehicle is a total loss when the cost to repair it exceeds a percentage of its value. The calculation method and ratio vary state to state. Some states use a flat percentage of the vehicle’s value as a threshold. Other states add the salvage or scrap value of the vehicle. That’s called the formula method. In general, it’s easier to total a vehicle using the formula method. That’s because the salvage value is added to the value of the vehicle before calculating the percentage.

Maine uses the formula method. Maine law considers a vehicle a total loss if the damage plus the scrap value exceeds 75% of the value.

For example:

Vehicle’s pre-loss Value

Repair Cost

Salvage Value

Repair + Salvage

Totaled?

$5280

$3150

$500

$3650

NO

$5280

$3650

$750

$4400

YES

My Car’s Worth More than the Repair Estimate. Why is it Totaled?

When an insurance company totals your car instead of paying the repair cost, they sell the salvage. The scrap value is considered part of the value of your vehicle. If it’s cheaper for the insurance company to pay you the value of your car and recover the salvage, they will. If it’s cheaper for them to repair your vehicle, they will do that.

In Maine, if the cost to repair plus the scrap value exceeds 75% of your vehicle’s value, the insurance company can total it.

Why 75%? Insurance companies know there’s often hidden damage after a serious loss. When the repair shop removes outer damaged parts, more damage is revealed. That increases the repair cost from their original estimate. So, insurance companies use 75% to provide a safety factor. That way, they’re not paying more to fix your vehicle than it’s worth.

Why Nicer Cars Are Easier to Total

High end cars cost more to fix. Their salvage value is also higher. So, the nicer your vehicle, the easier it is to reach the 75% threshold. A newer vehicle with a lot of cosmetic damage (e.g. hail) may have no mechanical issue and still be totaled. That’s because many expensive mechanical parts are still good, increasing the scrap value.

What Happens When My Vehicle is Totaled in Maine?

If your Maine vehicle is totaled, you essentially sell it to the insurance company. They pay you the pre-damage fair market value of the vehicle. You sign the title over to the insurance company. They keep the salvage value after selling it. Usually, it’s sold at auction.

Can You Keep Your Vehicle in Maine After It’s Totaled?

You can buy your unrepaired vehicle back from the insurance company for its salvage value. You still sell the vehicle to the insurance company by signing over the title. They pay you the pre-damage value of your vehicle, minus the salvage value. They sell you a Maine salvaged title for the salvage value.

Can I Drive a Vehicle With a Maine Salvaged Title?

No. Once there’s a salvage title, all of the work on the repair estimate MUST be done before you can drive the vehicle. You and the repair garage must complete and submit Form MVT-103 to Maine Bureau of Motor Vehicles.

When the State of Maine approves your vehicle repairs, it issues a rebuilt title. A rebuilt titled vehicle is worth less than one with a regular title.

Many insurance companies will not offer comprehensive or collision coverage for a vehicle with a rebuilt title. That’s because it can be difficult to assess the fair value of the vehicle.

The Insurance Company Wants to Total My Vehicle. Do I Have to Accept That?

You have the right to get your own repair estimate and choose your own body shop. Can you find one that will repair your vehicle for less than the threshold? Your insurance company might agree and pay the repair cost. Remember: in Maine, the 75% threshold includes the scrap value of your vehicle.

Once an insurance company totals your vehicle, you have a salvage title. You must repair the vehicle to drive it.

What if the damage is mostly cosmetic, and the car drives fine? You have the option to withdraw your claim and avoid a salvage title.

An Example of Withdrawing a Claim

Assume that a hailstorm pounds your vehicle. Dozens of dents on the hood, roof and trunk; a broken windshield. But the vehicle drives fine, and the dents don’t bother you. You could withdraw your insurance claim and pay to repair your windshield “out of pocket”. Although your vehicle may not look great, you might be able to drive it for many more years.

What if you withdraw your claim and don’t repair the body damage? Your insurance company will probably remove comprehensive and collision coverage. That’s because they wouldn’t pay for future damage; they already consider it totaled. Makes sense.

If you switch insurance companies, it’s important to declare the prior damage to them. The new insurance company will likely exclude comprehensive and collision coverage, too.

Questions About Maine Auto Insurance?

Do you live in Southern Maine and have questions about your auto insurance? Contact Noyes Hall & Allen Insurance in South Portland at 207-799-5541. We’re independent and committed to you. We offer a choice of Maine’s preferred auto insurance companies.

Small business owners are the heart of the American economy. Maybe you are not big enough to be listed on the Dow Jones Index, but your enterprise is what drives Main Street in towns across Maine. However, you should not get complacent. Small businesses are susceptible to lawsuits, workers compensation claims and other situations that they cannot handle as readily as large corporations. It is imperative that you have protection for these times.

To keep your business safe in times of adversity, you should consider comprehensive commercial insurance. Contact us at Noyes Hall & Allen Insurance to speak with one of our agents today.

Following are examples of commercial insurance that many small businesses in the Portland, ME region find beneficial, along with some factors used to decide which, and how much, insurance to purchase.

Liability

These policies can protect you when held liable for harm done to another.

A customer or supplier who comes into contact with your business may get injured or sick for example. You will then need funds to take care of medical bills or legal fees. Liability policies can help defray certain of these costs.

Commercial Auto

If your business uses vehicles to transport things or people, then you will probably need some commercial auto insurance.

It is best not to rely on your personal auto insurance, even if you do use your everyday car for these purposes. Commercial auto insurance policies usually cover situations that your personal auto insurance will not.

Errors and Omissions

It is imperative that professionals, such as lawyers, accountants, and others who work independently, have error and omissions insurance. These policies help individuals who provide services and dispense advice when they are charged with negligence.

As you never know when a client may be dissatisfied with your work, it is best to have adequate errors and omissions insurance in place at all times.

Factors to Consider Before Choosing a Policy:

Annual revenue

Location

Number of employees

Rent

Get More Information Today

Contact Noyes Hall & Allen Insurance today to learn more about specific commercial insurance policies in the Portland, ME area and beyond.

Are you looking for a commercial lease for your Maine business? Moving your business from home or a co-working space to your first real office? Expanding your retail footprint from Portland to Westbrook or Scarborough? Just looking for new space? Either way, negotiating and signing a lease is a big move. It’s also a big commitment. And a legal contract.

A new location is an exciting opportunity for your Maine business. It’s tempting to lock in a great location by quickly signing a lease. Be a smart business person. Review it with your attorney, accountant and insurance agent first. It can save you trouble during the term of your business lease.

Why a Written Lease is Important

It’s good to have a written lease. It’s a legal contract that you can refer to whenever you have questions about your space. It’s also in black-and-white, which reduces misunderstanding when conflicts arise. And, a written lease is easy to review with your trusted advisors.

Review Your Lease with Your Advisors – Before You Sign It

If you have an attorney, make sure they review your lease. They know what clauses are standard, and which are unusual in the Southern Maine market. They can help you negotiate with your potential landlord. Likewise, your accountant can determine tax implications of your lease. They can set you up to properly record your lease expenditures.

Don’t forget to review your lease with your Maine business insurance agent. Your lease requires property and liability business insurance. Your agent can help make sure you meet your lease obligations. They can also keep your property and other assets protected. Finally, they can help you build an insurance budget for your new location.

Insurance Implications of Your Commercial Lease

Depending on your operations and your lease agreement, you may need to update your business insurance. Here are a few examples.

BUSINESS PROPERTY INSURANCE AND YOUR LEASE

Insuring building items and improvements. Your new space may need a build-out. Who pays for that? Who insures it after it’s done? And who owns it, and when? A well-written lease addresses those issues.

A good Maine business insurance agent can help you determine whether you need to insure improvements. If you do, they can also tell you how much it will cost. Triple net leases require a tenant to assume many expenses of the building, including insurance. Your agent can help you budget for that.

Insuring Your Contents and Inventory Your new place may be larger, or be an additional location for your business. If so, increase your insurance to make sure that your assets are properly protected. Don’t forget to insurer new signage, awnings, etc.

In Case of Emergency What does your lease say about damage to the property? What if the property is damaged to the point where you can’t operate your business for some time? A well-crafted lease outlines the extent of damage and the time limit that triggers the clause.

It’s one thing for your lease to allow you to move somewhere else in case of damage to the property. It’s another thing to be able to afford to move, and to let your customers know about it. An astute Maine business insurance agent can help you buy insurance to pay for business interruption and extra expenses.

BUSINESS LIABILITY INSURANCE AND YOUR LEASE

Your lease may require a certain amount of business liability insurance protection. That may be more insurance than you currently have. You might even need business umbrella insurance to satisfy the lease requirements. Your commercial insurance agent can provide figures to build into your pro-forma for the new location.

Who’s Responsible for What? Your lease should outline what areas you are responsible for vs. the landlord. It may address issues such as maintenance and snow removal. Make sure that you know what your lease commits you to. Share that with your business insurance agent.

Hold Harmless Clause / Mutual Waiver of Subrogation Many commercial leases have a “hold harmless” clause. This prevents a landlord from suing a tenant or vice versa, except in cases of extreme negligence. These clauses help to maintain good relations between the parties. Instead of pointing fingers at each other, the landlord and tenant simply pay for damage to the property they’re responsible for in the lease. Many leases also have a “mutual waiver of subrogation.” This prevents the landlord and tenants’ insurance companies from collecting from an other at-fault party after they pay a claim. It’s important to share your lease with your insurance agent so they can make sure your insurance is properly set up.

Additional Insureds and Certificates of Insurance Many leases require tenants to make the landlord an Additional Insured under their policy. Insurance companies are generally willing to do this when required in a lease. Some insurance companies charge extra for Additional Insureds. Check with your business insurance agent to build your budget.

Does your new location have an exterior sign or outdoor seating area? The city or town may require a certificate of liability insurance showing them as an Additional Insured. Hanging signs and outdoor seating are popular in areas like the Old Port and downtown Westbrook, Biddeford and Saco. The city wants to make sure that if your sign injures someone, your insurance will pay. Overhead signs are also common in suburban strip retail areas, such as Scarborough, South Portland and Falmouth.

Are you looking for a commercial lease for your southern Maine business? Call Noyes Hall & Allen Insurance in South Portland at 207-799-5541. We offer a choice of many of Maine’s best business insurance companies. We can help make sure your insurance meets your lease requirements. We can also help you build your insurance budget for this location. We’re independent and committed to you.

Running your small Portland, ME business can be a rewarding and satisfying endeavor. However, without the right liability insurance coverage, running your small business open you up to lawsuits. Here is a brief description from Noyes Hall & Allen Insurance of the most common business liability insurance.

Worker’s Comp

Worker’s compensation insurance is required in Maine for any business with employees. As a business owner, you need to stay up to date on your state’s requirements concerning worker’s compensation insurance. Worker’s compensation insurance protects your employees when they are injured on the job. This also protects you as the employer from liability for said injuries.

Liability Insurance

General liability is one of the most important types of insurance for the small business owner to have. Liability can come in many forms. Individuals can get injured on your property or by your product. Something could go wrong with a service you provided resulting in damage or injury. Liability insurance will protect you in these situations and ensure that your company is not required to pay out of pocket for these types of liability claims.

Commercial Auto

If your company owns vehicles in order to provide services or deliveries, then you need business auto insurance. Commercial vehicle insurance can cover your drivers and your vehicles in the event of an accident. If your company uses vehicles, then you will no doubt have invested a good deal of money into those vehicles. This will protect that investment.

Umbrella Insurance

Commercial umbrella insurance policies help small business cover all their bases in one simple policy. Umbrella policies provide high limits of liabilty over your general liability and business auto policies. To learn more about small businesses, contact our friendly staff at Noyes Hall & Allen Insurance serving Portland, ME at 207-799-5541. We offer a choice of Maine’s best business insurance companies, so we can help you find the best value. We’re independent and committed to you.

We have invested in a new service for our clients: 24 x 7 access to your insurance documents from the Noyes Hall & Allen Insurance Client Center. Now you can view your secure policy information, download insurance cards and other proof of insurance, and request policy changes anytime. This 6:17 video explains how:

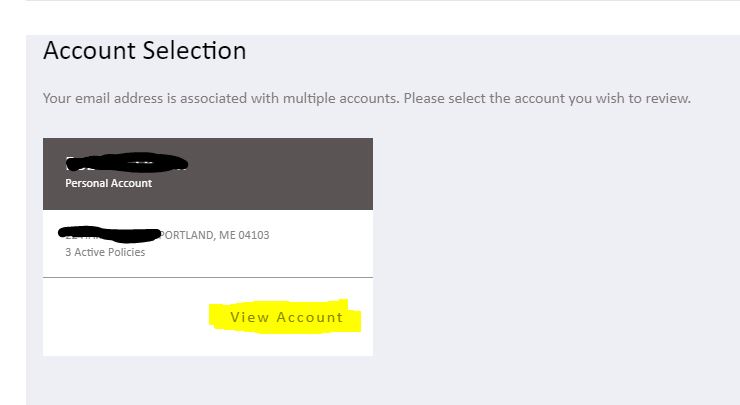

Log in to the Noyes Hall & Allen Client Center from our home page. Simply enter the email address associated with your account. We will email a one-time code. Enter it in the field, and you’re in! Note: some mobile users may have difficulty with certain browsers. We’ve found that Google Chrome works reliably with most devices.

Select View Account to see the information you want.

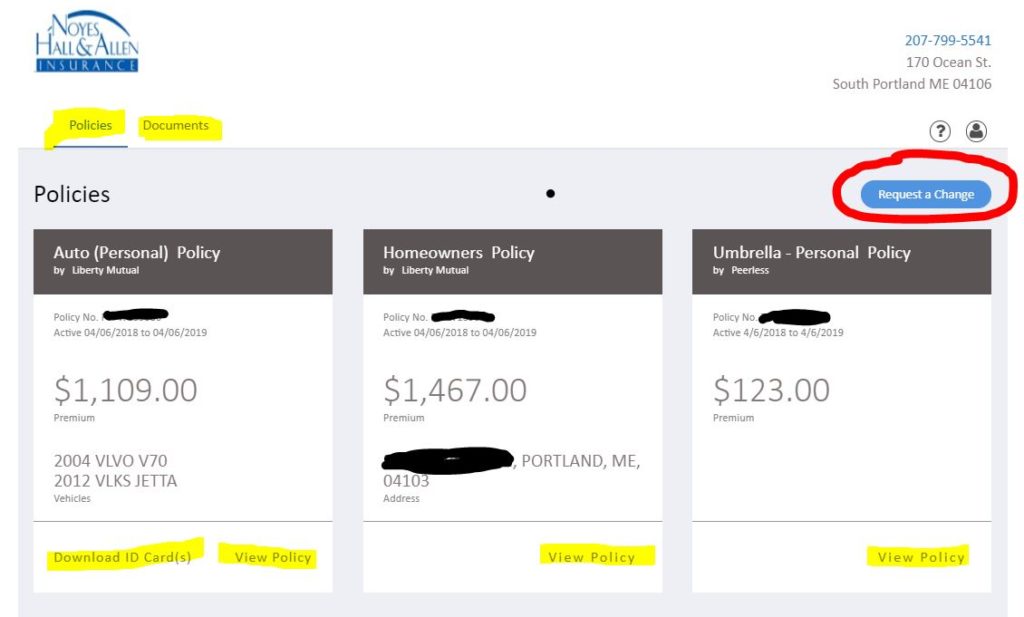

Select Policy to see your in-force policies and coverage info, or Documents to see or download proof of insurance, correspondence, or other information we have shared with you. Note that you can also request a change to your insurance policies from the Client Center.

When you’re done, you can log out by clicking on the person icon in the upper right, or simply closing your browser. Our vendor uses the latest security technology to keep your personal information private. You can view our privacy policy here.

THAT’S IT!

We hope you find the Noyes Hall & Allen Insurance Client Center useful to access your information when it’s convenient for you, whether the office is open or not.

Please note that these are very simplified views of your policy info. You may have purchased additional coverage which doesn’t show on the Client Center policy screen. Your actual insurance policy is always the definitive document of your coverage.

If you have any questions about your insurance, call a Noyes Hall & Allen agent at 207-799-5541. We’re independent and committed to you!

No one enjoys making an insurance claim. Something bad happened. You need it fixed. Soon. So much to do! Repair a car or building. Run a business. Get a temporary vehicle. Find a place to live or work. Heal from an injury. Replace damaged or stolen property. Deal with another party after the accident. Stress!

It’s an inconvenience you didn’t need. But, that’s why you bought insurance, right? It’s time for policy to do what it promises: fix you.

Insurance is a Two-Party Contract

Your insurance policy is a written contract between you and your insurance company. No one can change it after a claim. Your contract makes you responsible for certain things. The insurance company too. The policy specifies what’s covered, what’s not, and how losses are paid.

If you purchased your policy from an agent, they can help you through the process. But some things you have to do yourself.

Things only YOU can do in an insurance claim:

Make a statement about what happened to insurance companies

Prove your loss

Choose a contractor or repair shop (some companies have preferred contractors or shops, but cannot force you to use them)

Accept or reject a settlement

Things only your ADJUSTER can do in an insurance claim:

Determine whether your policy covers your loss

Decide who’s at fault in claims involving more than one party

Evaluate and pay claims

Some claims never involve anyone but you and the insurance company. You report it directly to the insurance company. The claim is minor. Settlement is simple. Everything goes smoothly. Other claims are more complex.

You never know which kind of claim you will have. That’s why it’s good to have an agent on your side. Not to mention for the advice they can give you the 99.9% of the time when you’re NOT having a claim.

What Use Is an INSURANCE AGENT after a Claim?

A good insurance agent:

Helps you decide whether to make a claim at all. Is your claim clearly not covered? If it is clearly covered, what’s your policy deductible? Is your insurance cost likely to increase if you make this claim? How much? An agent can answer these initial questions so you can decide whether you want to make a claim at all.

Is your insurance sherpa. There’s a lot to know and remember. Report your claim to your insurance company or someone else’s. Protect your property. Gather information you’ll need later. Find a temporary solution until the adjuster can take over. An experienced agent is your sherpa in foreign territory.

Is your claim cattle dog. Haven’t heard from your adjuster? Waiting for an appraisal? Having trouble preparing the reports the insurance company needs? A good agent can pull things together and herd your claim in the right direction.

Has clout with the insurance company. Agents help their clients to find good insurance companies. So insurers want to be on the agent’s “good list”. A trustworthy and knowledgeable agent earns the respect of the insurance company. They can use that to advocate on your behalf. An agent can’t create coverage where there isn’t, but they can influence the process.

Is an “insurance translator”. A good agent can explain the gobbledy-gook in that letter from your adjuster. They can tell you why the offered settlement may be different than you expected. They can explain to the adjuster, using insurance terms, it if it’s wrong. Your agent can even translate in real time, meeting with you and the adjuster face-to-face, to resolve issues.

Helps insurance companies get better. Want to let your insurance company know how your claim went? Compliment your adjuster? Complain about the company’s preferred service provider? Rave or rage about the service you received? Share advice for how to make it better? A good agent has a pipeline to the insurance company, and knows where to send the feedback to get the most impact.

Need Help With a Claim? Ask Your Agent!

Don’t assume that your agent knows how your claim is going. Insurance companies don’t routinely communicate with agents during a claim. If you need help, ask your agent. At Noyes Hall & Allen Insurance, we ask our clients if they need help a week after they file a claim on their policy. Many don’t need help. But for those who do we’re able to jump in and assist where needed. We believe that helps our clients’ claims go smoother than they might otherwise.

Do you own a business or live in the Portland Maine area? Looking for an experienced agent who represents several insurance companies? An agent who can help you choose the right insurer and be available if you have a claim? Contact a Noyes Hall & Allen Insurance agent in South Portland at 207-799-5541. Or just click “get a quote” above. We offer a choice of Maine’s preferred business and personal insurance companies. We’re independent and committed to you.

Food trucks have roamed the streets of Portland Maine for several years. Now they’re popping up in places from Biddeford Saco to Westbrook, Scarborough to Freeport, Sugarloaf to Sunday River. Food truck insurance can be a challenge for an inexperienced insurance agent. Insurance companies know how to insure trucks. They know how to insure restaurants. But rolling restaurants are different.

5 Types of Insurance Every Food Truck Needs

General Liability Insurance

If someone breaks a tooth in a crabmeat roll or gets food poisoning after eating your product, they’re going to come back to you. GL coverage pays for these claims, as well as slips and falls and other injuries or damage that occur at your location.

Business Auto Insurance

If you get in an accident while you’re on the move, you need to have your food truck fixed and back online soon. If you’re at fault, you’ll also need protection to pay for the damage and injury you cause.

Workers Compensation Insurance

By law, you’re required to provide Maine workers comp coverage for your employees. If they’re injured at work or miss time due to an on-the-job injury or illness, workers compensation insurance pays them.

Business Property Insurance

You have a big investment in your inventory, fixtures and supplies, both at the commissary and on your food truck. Insurance can protect that asset against fire, theft, equipment breakdown and more.

Loss Of Food Truck Income

If your food truck is down, you have no income. What if your fryer malfunctions, causing a fire? You could be off the road for the whole summer season. Or what if your best brewery location or outdoor venue suddenly shuts down due to a fire, windstorm or some other disaster? Business income insurance for food trucks can help you replace the income you lose following property losses like these.

Get Maine Food Truck Insurance

If you have questions about insuring a food truck in Maine, contact a Noyes Hall & Allen insurancce agent in South Portland at 207-799-5541, or click “get a quote” above. We’ve insured food trucks since they first came to Maine. We offer a choice of Maine’s preferred insurance companies, including the Acadia Street Eats food truck program by Acadia Insurance. We’ll help you find an insurance solution that fits your business and your budget. We’re independent and committed to you.